Libor Phase-Out Still Leaves New Deals at Risk, Moody's Says

Libor Phase-Out Still Leaves New Deals at Risk, Moody's Says

(Bloomberg) -- Regulators and issuers of bonds backed by consumer or corporate debt are taking steps to address the Libor phase-out, but new deals have transition risk that could hurt their credit quality, according to Moody’s Investors Service.

Language added to bond deals after 2017 “significantly reduces” the potential for floating-rate transactions to become fixed if Libor is phased out, according to a report released Thursday. But collateralized loan obligations, student-loan backed debt and notes based on streams of home rental payments may face additional risks because they are exposed to the benchmark via their bonds as well as the assets and derivatives backing the securities.

“Although the widespread introduction of new documentation and other preparation has been broadly credit positive, it has not eliminated Libor transition risks for new structured finance deals," analysts led by Jody Shenn wrote in the note. There’s “significant uncertainty and complexities confronting market participants,” they said.

In some securities, different rates could end up referencing the bonds and underlying assets when Libor is eliminated, raising the possibility that incoming and outgoing cash flows will no longer match. If more money is flowing out of the securities than into them, the bonds could see reduced investor protections or interest shortfalls, according to Moody’s. Some deals could also see unexpected legal expenses tied to the transition, and it’s also possible that borrowing costs could rise or become more volatile, increasing default rates.

The move away from Libor is “unlikely to intentionally raise payments materially” for issuers, the analysts said, though the bonds could also be hurt if uncertainty around the process or difficulty hedging reduces market liquidity, they said.

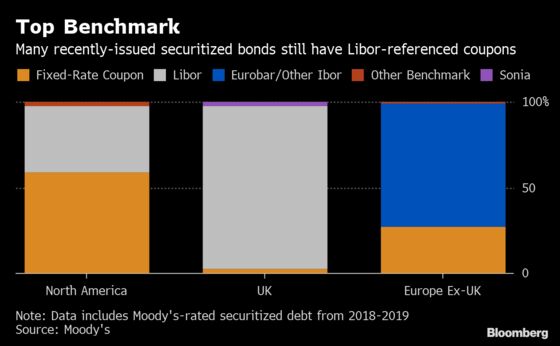

Most deals issued after 2017 haven’t selected an alternative benchmark like the Secured Overnight Financing Rate in the U.S. or the U.K.’s Sterling Overnight Index Average, Moody’s said. Instead, the documents include language addressing when and how a Libor transition should be handled, which should help support the bonds. Many affected bonds are also shorter-duration and should be paid down or close to being paid down before 2021, when the rate is set to be phased out.

Some of the transition risks should be mitigated because bond issuers have an incentive to protect investors so they can maintain access to the markets, the analysts said. This should entice issuers to “align new benchmarks for bonds and assets to the degree those decisions are under their control” instead of “making decisions that are the most economically advantageous to them,” the analysts wrote. Sponsors may also opt to call bonds early if deals tied to Libor would likely see their creditworthiness suffer during the benchmark transition, they said.

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Christopher DeReza

©2019 Bloomberg L.P.