The Leveraged Loan-Junk Bond Quandary Is Just a Rates Trade

The Leveraged Loan-Junk Bond Quandary Is Just a Rates Trade

(Bloomberg Opinion) -- Every once in a while, there’s a market anomaly that simply hits investors over the head. The latest such episode comes from the riskiest corners of the U.S. corporate debt market.

The yields on junk bonds have collapsed relative to those on leveraged loans. Bloomberg News’s Lisa Lee and Sally Bakewell published their analysis on Thursday at 6 a.m. New York time:

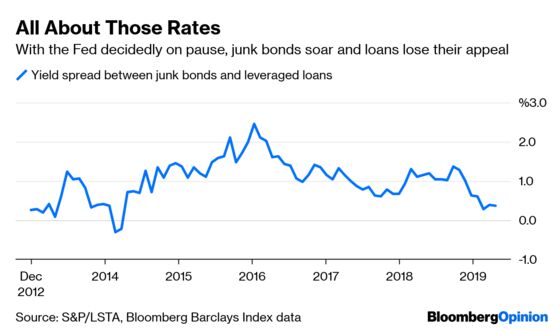

While high-yield bond prices have been surging, loans to junk-rated companies have been lagging, leaving the gap in yields between the two types of debt at just 0.39 percentage point through Tuesday, around the narrowest since 2014. Investors are now willing to accept little or no extra compensation for buying bonds, which are in theory riskier than loans to similar corporations.

In case you missed that, though, precisely two hours later, The Wall Street Journal had its own perspective, in an article titled “Fed Shift Shakes Up World of Speculative Debt.”

Bond yields, which move in the opposite direction of prices, typically exceed those of loans because holders of the latter are typically paid first in bankruptcies. This year, yields on both are down amid a broad rally in riskier assets…

Some consider the extra yield that investors are demanding to hold loans over bonds to be surprising. Despite a recent uptick in issuance of secured bonds that would be ranked equal to loans in a bankruptcy proceeding, most bonds are unsecured, meaning their holders are at greater risk of losses if the companies that have issued them encounter financial stress. That is why average loan yields have been lower than average bond yields for the vast majority of time since a market for loans emerged in the 1990s.

And now you’re reading it again in this column. The development is noteworthy, to be sure, especially because of all the heavyweights who cautioned against froth in leveraged lending. At the same time, those same people have been quiet as of late. That’s because the Federal Reserve’s abrupt shift away from further interest-rate increases has quashed the appeal of loans. And that might be an understatement — individual investors have pulled money from leveraged-loan funds for a whopping 23 consecutive weeks.

Effectively, the convergence of yields on loans and junk bonds boils down to a trade based on interest-rate expectations, somewhat similar to how the Treasury yield curve steepens or flattens. All else equal, if the Fed is more likely to cut its benchmark than raise it, investors would be smart to snap up the higher fixed rates on bonds, rather than be caught holding loans that can get refinanced at a lower coupon. That’s a similar logic to purchasing five-year Treasuries at a yield lower than those due in a year — the reinvestment risk is too great.

Of course, it’s a bit more complicated because loans and bonds typically have different priority in cases of distress. But even that distinction is murky at best, after an increasing share of companies in recent years tapped the leveraged-loan market without any unsecured bonds beneath them to shield loan buyers from losses. Moody’s Investors Service earlier this year declared that leveraged loans were “now in uncharted territory” as far as deteriorating investor protections.

Frank Ossino, portfolio manager at Newfleet Asset Management, talked to both publications and argued that the yield convergence was little more than a “technical dislocation.” He said he favored rotating into loans because they’re relatively cheap. Loans are certainly cheaper relative to high-yield debt than before, but it’s an open question whether they’re outright cheap. As Lee and Bakewell put it, this is far from a slam-dunk trade, both because of the refinancing risk and the prospect of weaker recovery rates than the historical average.

On balance, this yield convergence feels as if it could last a while. Even though traders are increasingly hedging for a potential Fed interest-rate cut, it seems more likely that Chairman Jerome Powell and other policy makers will just stay out of the market’s way and hold the bank’s benchmark lending rate steady for as long as they can. That could leave both junk bonds and leveraged loans plodding along. This is one anomaly that has no clear easy-money answer.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.