Lebanese Default Risk Prompts Moody's Downgrade Deeper Into Junk

Lebanon's Debt Urgency Prompts Moody's Downgrade on Default Risk

(Bloomberg) -- Lebanon wasn’t spared a debt rating downgrade that pushed it deeper into junk, hours after Qatar unveiled a plan to plow $500 million into its government bonds.

Moody’s Investors Service lowered the country’s credit score one step to Caa1, seven levels below investment grade and on par with countries including Gabon, Zambia and Iraq. It changed the outlook to stable from negative.

Even though Lebanon’s caretaker government has disavowed any debt restructuring, recent official comments suggest “a growing urgency” that coping with one of the world’s biggest debt burdens might prompt measures resulting “in a default event under Moody’s definition,” according to a statement on Tuesday.

Eight months on from an election, Lebanon remains without a government and with billions of dollars in aid untapped as sectarian tensions simmer. The central bank has maintained stability through stimulus measures and financial engineering, made possible by the billions of dollars deposited into Lebanese banks by the nation’s diaspora.

While Moody’s report highlights the need to form the government more quickly and embark on reforms, Finance Minister Ali Hasan Khalil said that “the financial and monetary situation remains stable, the needs of the Treasury are secure, and it’s able to meet all commitments, especially on debt.” Lebanon is hopeful Qatar’s decision is a “prelude” to a show of support by other countries and institutions, he said on Twitter.

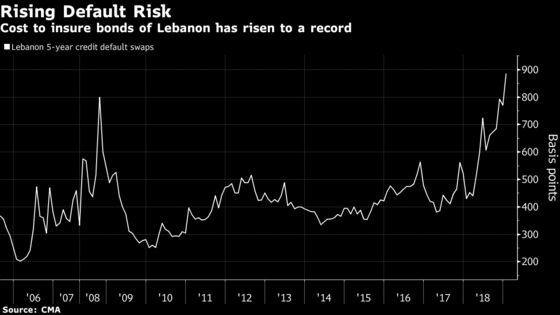

Bonds Gyrate

While Eurobonds rallied on Monday after Qatar’s announcement of its cash infusion, relief was short-lived. The yield on Lebanon’s dollar debt due 2021 jumped 26 basis points to 14.31 percent as of 1:59 p.m. in Beirut on Tuesday. It reached 14.86 percent on Jan. 18, the highest on a closing basis since the bonds were issued in 2006.

The nation’s five-year credit-default swaps have climbed 15 percent this year, the most among contracts tracked by Bloomberg globally.

The latest wave of concern over Lebanon’s tottering finances and political deadlock was sparked this month when its finance minister roiled bond markets by telling a newspaper the government was considering restructuring its debt.

Trying to clear up confusion and calm investor nerves, he said later that while a fiscal program doesn’t include a restructuring, it may entail a rescheduling of debt. Other top officials have also stressed that Lebanon was discussing how to reduce the budget deficit and implement reforms -- but would not restructure its debt.

‘Heightened Risk’

For Moody’s, however, the distinction may be moot. In its statement, the rating company pointed to “the heightened risk that the government’s response to increased liquidity and financial stability risks will include a debt rescheduling or other liability management exercise that may constitute a default under Moody’s definition.”

Lebanon’s debt burden reached 141 percent of gross domestic product in 2018, excluding domestic liabilities of public entities, and the cost of servicing it is equivalent to almost half of government revenue, Moody’s estimates.

Starting in 2016, commercial lenders have been encouraged to draw new deposits and park their liquid foreign assets at the central bank. While deposit inflows have slowed and reached an estimated $4 billion to $5 billion in 2018, Moody’s said Lebanon would need as much as $7 billion to cover this year’s fiscal deficit and Eurobond maturities without tapping foreign-exchange reserves.

Goldman Sachs Group Inc. said in a January report that foreign investors would recover 35 cents on the dollar under the bank’s base scenario, even though it sees an imminent debt restructuring as unlikely. Like Moody’s, Fitch Ratings also lowered the outlook on the country’s B- credit score to negative in December.

“While some mandates don’t allow holding of CCC rated securities, we think that conservative investors may have already reduced their Lebanon exposure; this limited forced selling,” Jaiparan Khurana, a London-based strategist at Morgan Stanley, wrote in a note. “That said, as the downgrade limits the investor base it should still weigh on the long end.”

--With assistance from Abbas Al Lawati.

To contact the reporters on this story: Lilian Karunungan in Singapore at lkarunungan@bloomberg.net;Netty Ismail in Dubai at nismail3@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, Paul Abelsky, Alex Nicholson

©2019 Bloomberg L.P.