Lame Monetary Policy Leaves MMT as Top Catalyst for Inflation

Lame Monetary Policy Leaves MMT as Top Catalyst for Inflation

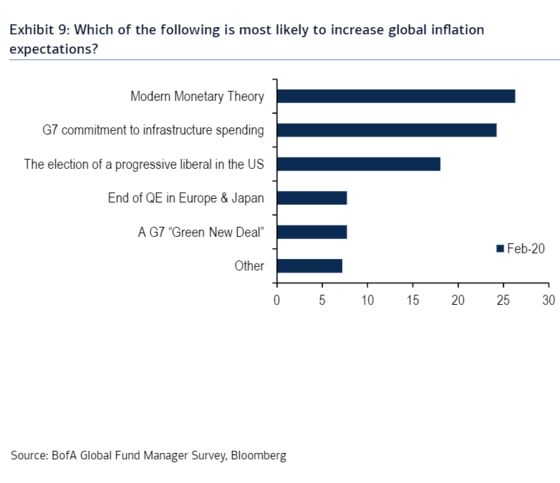

(Bloomberg) -- The current era of persistently low inflation is most likely to be reversed by Modern Monetary Theory, according to fund managers with $632 billion in assets, a development which could also reverse the stock market’s winners and losers.

A full-scale embrace of MMT by fiscal policy makers would likely entail an increase in labor and resource utilization, which could put upward pressure on wages and prices. This response from Wall Street to the February survey of global investors conducted by Bank of America Corp. reinforces the deepening skepticism over the ability of monetary policy to spur inflation on its own, and a creeping recognition that more muscular action from government may be required to bolster aggregate demand and price pressures.

MMT, its proponents contend, is a lens through which the economy can be analyzed rather than a specific set of policy prescriptions. This way of looking at the world preaches that governments that borrow in their own sovereign currencies can’t default and therefore do not face a budget constraint, but are limited by real resources. In the U.S., MMT has become somewhat intertwined with a calls for a job guarantee and broader Green New Deal thanks to politicians like Representative Alexandria Ocasio-Cortez and Senator Bernie Sanders.

While Wall Street economists have mixed feelings on the merits of MMT, the concept has drawn sharp criticism from luminaries like Berkshire Hathaway Inc. Chief Executive Officer Warren Buffett and Federal Reserve Chair Jerome Powell.

Stony Brook University Professor Stephanie Kelton, an adviser to Sanders’ presidential campaign and the public face of MMT, suggested that the U.S. budget deficit could safely increase by another $500 billion before beginning to spark “problematic” price pressures. MMT is not in favor of runaway inflation. Some of its leading proponents have indicated that while an inflation constraint is preferable to a budget constraint for governments, inflation isn’t always an indication of an overheating economy. Since sources of inflation can be relatively concentrated and independent of the business cycle, regulatory policy may thus be a more effective lever to pull to control inflation, they argue.

The persistently sluggish global recovery from the Great Recession despite an onslaught of central bank easing has had profound effects on financial markets, which helps explain investors’ belief that more structural changes would be necessary to materially alter the macroeconomic environment. Ten-year measures of market based inflation compensation have routinely run below what would be consistent with the Federal Reserve achieving its 2% target for most of the expansion.

The relative return from value stocks versus their growth counterparts has sunk to its lowest level since the dot-com bubble as investors piled into the small number of superstar firms and industries able to buck the global malaise by posting consistently above-trend growth -- at ever-escalating equity valuations.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka, Rita Nazareth

©2020 Bloomberg L.P.