Kraft Heinz's Warning to Its Financial Imitators

Kraft Heinz's Warning to Its Financial Imitators

(Bloomberg Opinion) -- It’s not just in haute couture that fashions change.

In the grocery aisle, trends also come go, and we’re not just talking about consumers turning off of processed foods and choosing niche items instead.

Thanks to the poor performances of Kraft Heinz Co. and Anheuser-Busch InBev SA, investors’ appetites are also changing: from a demand for fatter profits, even if sales growth is sluggish, to a strategy that better balances the top and bottom lines, and is backed by a solid balance sheet, not one loaded with debt.

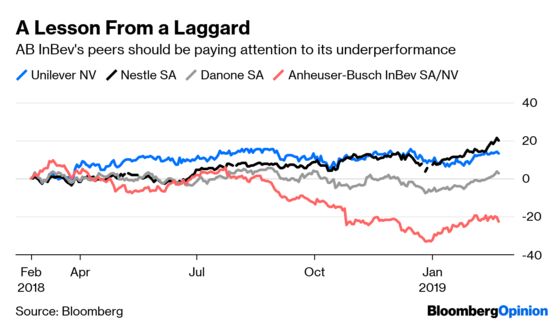

Kraft Heinz’s ugly earnings report on Thursday, its $15 billion write-down on some of its best known brands and an accounting subpoena look like the final nail in the margin-chasing coffin. The likes of Unilever Plc and Nestle SA should take note.

To recap: five years ago the big consumer groups were hit by slowing sales, driven by emerging markets running out of steam and consumers moving away from big, well known brands to more fresh and locally produced food. Boards turned their attention to increasing profits instead, necessitating big cost savings.

The leaders of the margin muscle gang were Kraft Heinz and AB InBev. Brazilian investment firm 3G Capital, with help from Warren Buffett, combined Kraft and Heinz in 2015. They set about slashing costs and lifting operating margins from a typical range of 15 percent to 18 percent before the merger, to as much as 28 percent in 2017.

It was a similar picture at AB InBev, which counts 3G Capital’s founders among its largest shareholders. After a long chase it finally clinched SAB Miller for about $100 billion in 2016. The plan was to use its deal-making prowess, and its ability to strip out expenses, to expand its industry-leading margins and pay down debt.

The prospect of fatter profits at the two groups had shareholders salivating. Add in interest from activist investors in the consumer goods sector, and rivals all reacted.

Unilever, which repelled an approach from Kraft Heinz in February 2017, Nestle and Danone SA all subsequently set margin targets, putting a more formal focus on the measure.

But now, investors are having a rethink.

Even before this week’s announcement, Kraft Heinz’s performance had been uninspiring. Including Thursday’s fall, the shares are down almost 30 percent in the past year.

As for AB InBev, it has cut its dividend as it battles to revive sales in the U.S. and cope with unfavorable exchange rates in emerging markets. It is lumbering under a net debt load of about $100 billion, and its shares have dropped more than 20 percent over the past year.

Other big groups are going to have to respond. Amid this altered landscape, Nestle probably has the balance about right. Although he unveiled a margin target in autumn 2017, Chief Executive Officer Mark Schneider has said he wants Nestle’s strategy to steer a middle course between one that focuses on lifting profit at the expense of top line growth, and the sort of model that is pursued by revenue generating but loss-making start-ups. That approach might have appeared unexciting at the time, but now it looks smart. It helps that Nestle is already delivering on both its profit and growth goals.

Danone needs everything to go right this year to meet its 2020 aspirations. But it could achieve them.

As for Reckitt Benckiser Group Plc, another company with leading margins thanks to its focus on efficiencies, investors are concerned that it may have to bring down profit expectations in order to reinvigorate sales growth.

But perhaps Unilever is the company with the most at stake.

In one respect, it can breathe a sigh of relief. While another bid from Kraft Heinz was already looking unlikely – its market capitalization had already sunk below that of Unilever – now its one-time predator is even more debilitated.

The group nevertheless should be rethinking its strategy. Alan Jope had the opportunity to back off from his predecessor’s margin target when he became CEO in January, and instead shift the focus to turbocharging revenue. He didn’t take it. Instead, he’s stuck with plans to lift the operating margin to 20 percent by next year, while delivering underlying sales growth of between 3 percent and 5 percent.

That looks a stretch. While Unilever made progress on margins in 2018, sales growth was at the bottom of its 3-5 percent range.

The debacle at Kraft Heinz gives him another chance to reset expectations. He should take it.

Investors' priorities have shifted towards a better balance between sales and profit growth. Big consumer groups need to pivot once more.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.