Junk Winner in 2008 Trawls for Riches in 2020’s Illiquid Markets

Junk Winner in 2008 Trawls for Riches in 2020’s Illiquid Markets

(Bloomberg) -- Like many of his peers, Geof Marshall would love to buy the cheapest corporate bonds in decades, if he could get his hands on them.

But these are some of the strangest times Marshall has seen in a 21-year career investing in junk debt. Trading conditions have been frozen like never before, as an oil crash collides into the coronavirus crisis. Even would-be short-sellers are sidelined because of fear they won’t be able to exit positions down the road.

“This is like the bastard love child of 2008 and a market flash crash,” said the fixed-income chief at CI Investments’ Signature Global Asset Management with C$30 billion ($21 billion) which he runs from Toronto. “Traders are hamstrung. Not being able to cover shorts is just as scary as being long and unable to sell.”

Marshall, whose high-yield bets outperformed in 2009, is now scooping up easier-to-trade corporate debt getting pushed out of investment-grade indexes. Bets on so-called fallen angels could eventually notch billions for active managers fast off the block, if past performance is a guide.

“When we get fallen angels and the market gets dislocated, they get dislocated and very attractive,” Marshall said.

One of the fastest credit sell-offs in history has stoked fear, illiquidity and disruptions across fixed income.

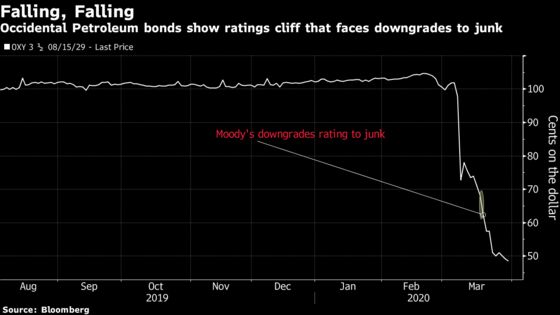

Take Occidental Petroleum Corp. As the energy crisis rages, the oil company’s $1.5 billion of 3.5% notes due 2029 have lost more than half their value this month amid a downgrade into junk. It’s among the first wave of fallen-angel downgrades that could total as much as $300 billion this year, according to Citigroup Inc.

Marshall sees a faster market recovery compared to the crisis this time round after policy makers moved quickly to keep money flowing to virus-shocked economies. The Federal Reserve also looks poised to prop up corporate bonds in its most expansive quantitative-easing program ever.

The fund manager has profited in these situations before. Marshall’s financial-crisis bets helped the Signature Global Income & Growth Fund that he co-manages with colleagues generate a 25% return in 2009 versus 17% for the Bloomberg Barclays Global Aggregate Credit Index.

Once the crisis passes, a slew of fallen angels look set to outperform, and relegated issuers are often the fastest to climb out of speculative-grade indexes. Over the past decade, downgraded names have far outperformed regular peers, according to analysis by Marty Fridson of Lehmann Livian Fridson Advisors LLC.

Yet charting the course of a global downturn that’s only just starting, and investing through it, might be harder than in the slower burning 2008 melt-down.

Even if the downturn is short, a 6.8% speculative-grade default rate is the best-case scenario, up from 3% in February, according to Moody’s Investors Service. Under conditions akin to those in the financial crisis, 16% of high-yield bonds could default. That could climb to 20% in a recession worse than 2008, the ratings firm said in a March 27 statement.

“The combination of the downgrades plus market dislocation equals some great opportunities,” Marshall said. Of course, “some of them will be falling knives.”

©2020 Bloomberg L.P.