JPMorgan Sees Gulf Bond Sales Slipping as Rates, Volatility Rise

JPMorgan Sees Gulf Bond Sales Slipping as Rates, Volatility Rise

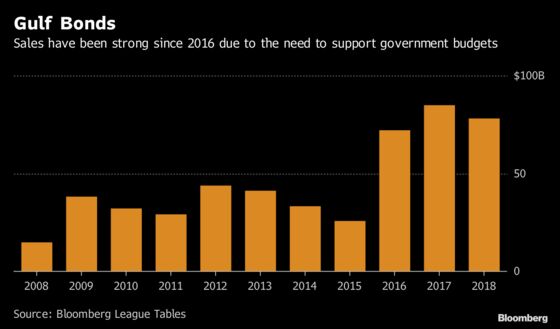

(Bloomberg) -- JPMorgan Chase & Co., one of the biggest arrangers of Gulf bond deals, expects sales to slip in 2019 from last year’s $78 billion as issuers turn cautious amid rising interest rates and market volatility.

In the past, when there has been uncertainty either “in rates or in spreads, regional issuers tended to become more careful and price sensitive,” Hani Deaibes, the U.S. bank’s regional head of debt capital markets, said in a phone interview from Dubai. “Most of our clients have multiple funding options and will consider other alternatives” if bonds turn too expensive, he said.

Borrowers from the six-nation Gulf Cooperation Council, which include the two biggest Arab economies of Saudi Arabia and the United Arab Emirates, primarily sell bonds in dollars and two further interest rate hikes forecast in the U.S. this year will add to costs. The possibility of economic growth stalling in the U.S. and China, the trade dispute between the world’s two biggest economies, political turmoil in Europe and falling oil prices are all contributing to volatility in financial markets that will make potential issuers uncomfortable.

GCC bond sales got off to a robust start this year as Saudi Arabia raised $7.5 billion from a two-part deal on Jan. 10. JPMorgan, the fourth biggest arranger of GCC bond sales in 2018, was one of five managers.

Prospective issuers may turn to bank loans for funding if bond-market volatility increases. GCC syndicated loans surged 54 percent to $114.5 billion last year, when foreign and local banks were flush with liquidity.

Deaibes also said:

- “It’s difficult to expect similar volume this year than in 2018”

- About $20 billion of bonds mature in 2019, while new issuance will be higher, so there is still “the need for international investors to keep investing in the region”

- Government fiscal deficits are the biggest driver of sovereign issuance

- “Saudi Arabia has flagged its intention for 2019; the question will be around the other regional sovereigns. If they come in large quantum then there will be greater probability that we would get to last year’s number but from where we stand today, it doesn’t seem to be the case. We are in a better position from a fiscal perspective, subject of course to oil prices”

- “Corporate issuance will be driven by refinancing, mergers and acquisitions, capital expenditure funding”

- Doesn’t expect an increase in issuance in 2019 driven by refinancing or capex, but M&A-driven supply is less predictable and could have a more material impact

- “Financial institutions have always been regular issuers, although they are relying more on private placements; fixed-income issuance will be subject to growth in the region”

To contact the reporter on this story: Arif Sharif in Dubai at asharif2@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Robert Brand, John Viljoen

©2019 Bloomberg L.P.