JPMorgan’s Michele Shuns Treasuries Turned ‘Zombies’ in QE Era

JPMorgan’s Michele Shuns Treasuries Turned ‘Zombies’ in QE Era

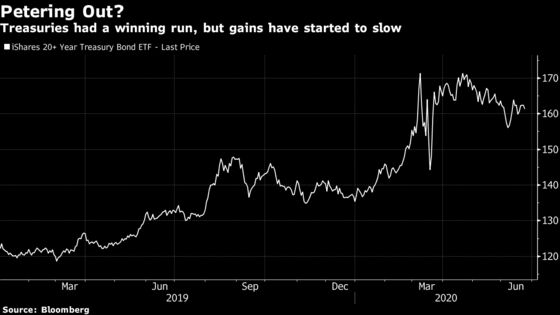

(Bloomberg) -- Bob Michele bet on U.S. yields sinking to zero last year, and reaped the rewards of a historic rally. Now, he says the gains are looking exhausted.

The chief investment officer and head of global fixed income at JPMorgan Asset Management has slashed the firm’s holdings of U.S. government bonds to the smallest since September 2018. He expects stagnant returns for the safest government bonds as global economies recover from coronavirus-induced recessions, and has pivoted into securities like corporate bonds and emerging markets debt pegged to growth.

Central bankers in the U.S., U.K., Germany and Australia are turning government debt into “zombie” bonds -- depriving them of the yield and volatility that makes them alluring to traders, Michele contends.

“We are going to be stuck with low yields for a long period of time,” Michele said in an interview. “Central banks are going to just control the level of yields in those markets and there are other things to us that look more attractive where we still get high quality and protection on the downside.”

The Federal Reserve and other central banks have pledged trillions in quantitative easing program to underpin economies hit by the pandemic. It’s possible that yields could fall further, Michele said. A spike in infections, election risk or even another rate cut would spark a flight to quality back to government bonds.

JPMorgan Fund That Sold Junk Debt Before Crash Is Diving Back In

The writing was on the wall for Michele in July 2019. While he didn’t warn a pandemic would bring global economies to a screeching halt, he did expect central banks to “cut rates as far as they can and expand balance sheets” to stave off a downturn.

Though the firm’s absolute holdings of Treasuries are the lowest in two years, duration, or exposure to rate risk though long-dated debt, is little changed.

“We are still holding roughly the same duration because we still expect yields to continue to come down,” Michele said. “Although we expect this recovery to continue and policy makers to ensure that it does, when you go back and look at the previous crises, there were fits and starts along the way.”

JPMorgan Asset now sees an 80% probability of above-trend global growth in the third quarter, compared with zero in the previous three months. The firm has also revised down a chance of a recession to 10% from 55%.

Growth Optimism

His optimistic view on the economy is one reason Michele favors securitized credit -- a choice he said surprised some of the company’s clients because it’s tied to consumer loans.

“Although the unemployment data looks horrific now, because of the policy response there’s enough cash coming to those collecting unemployment insurance that they are able to make payments on all the borrowing they have, and by and large they are doing it,” said Michele. “That’s been a pleasant surprise to us.”

Renewed trade tension between the U.S. and China poses the biggest threat to growth, overshadowing the risk of a second wave of Covid-19 and the U.S. election, he said.

“Elections come and go. They can be disruptive and create some political headwinds, but the market learns to reprice and adjust,” Michele said. “The world’s two biggest economies entering a feared cold war and the knock-on effects on the global economy is a long-term risk I am most concerned about.”

©2020 Bloomberg L.P.