JPMorgan’s Kolanovic Sees Pivot Back to Stocks by End of August

JPMorgan’s Kolanovic Sees Pivot Back to Stocks by End of August

(Bloomberg) -- U.S. equity investors who have been whipsawed for most of August can look forward to a reprieve in the next couple of weeks, JPMorgan Chase & Co.’s quant guru says.

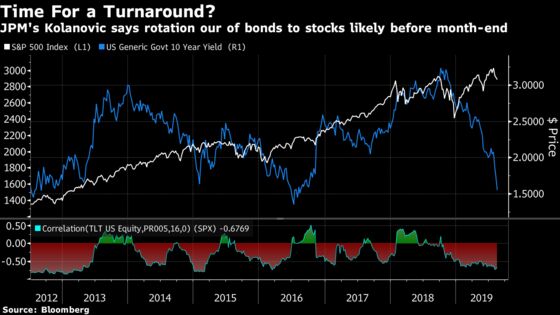

After Treasuries rose and the S&P 500 Index fell for three consecutive weeks, the divergence left fixed portfolios 2% underweight stocks, according to Marko Kolanovic, the bank’s head of macro quantitative and derivatives research. They’re likely to rotate back into equities to re-balance before the month is over, and that shift could push stocks 1.5% to 2% higher, he said.

In a week when the key part of the yield curve inverted and recession fear sparked an equity rout, systematic strategies posted $75 billion of programmatic selling, more than half of which came from index option delta and gamma hedging, JPMorgan’s analysis found. The rout pushed hedge funds’ equity exposure to near record lows and that of trend-following and volatility-targeting funds to the 27th percentile relative to history. Such low positioning is a positive signal for stock performance, according to Kolanovic.

“We expect some stabilization in market volatility as dealers’ gamma positioning is now close to neutral (from a sizable short position last week), and this may reduce volatility and marginally improve liquidity,” Kolanovic said in a note to clients on Tuesday. “Equity flows will to a large extent be driven by developments around trade, and hence the market will likely continue to be dominated by market disruptive tweets and announcements related to the trade war.”

While economic and macro concerns were partly responsible for the recent market rout, they took a backseat to technicals. More than half of last week’s price action that first sent the S&P 500 reeling and then triggered an impressive rebound was convexity hedging of mortgages and variable annuities, according to Kolanovic. He echoed research of his colleagues led by Josh Younger, who last week said that convexity hedging has totaled roughly $90 million per basis-point move in bond yields since the end of last month.

Mortgages have negative convexity, and for large investors that hold them, a drop in interest rates means the duration of these portfolios goes down. This leaves the holders scrambling to compensate by adding duration to their holdings.

To contact the reporter on this story: Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Richard Richtmyer, Dave Liedtka

©2019 Bloomberg L.P.