JPMorgan Joins UBS, BNP in Slashing Treasury Yield Forecasts

JPMorgan Joins UBS, BNP in Slashing Treasury Yield Forecasts

(Bloomberg) -- Strategists are catching up with falling Treasury yields.

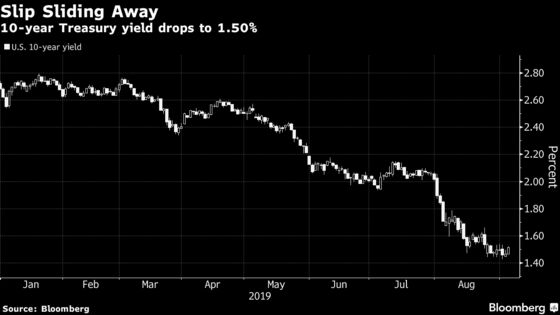

When the benchmark yield slid more than 50 basis points in August to 1.50%, it matched or surpassed many a year-end forecast. Now bond experts from BNP Paribas SA to JPMorgan Chase & Co. are cutting their numbers to reflect the global slump in yields, as clouds gather over the world economy.

“We’ve taken our rates forecasts lower as the market has got to our target quicker than we thought -- and for good reason, given our analysis of the macro situation,” BNP head of Group-of-10 rates strategy for the Americas Shahid Ladha said in a phone interview. The French bank slashed its end-of-year forecast for the 10-year U.S. yield to 1% from 1.75% in its fourth-quarter outlook.

UBS Group AG’s global macro strategists including Matthew Johnson and Chirag Mirani have also penciled in a decline to 1%, even though the benchmark hadn’t yet reached their previous forecast of 1.25%. Both BNP and UBS cited a slowing global economy as the impetus behind their changes.

The escalating U.S.-China trade war and a slew of disappointing economic data have ignited a global bond rally sending Treasury yields sliding. Geopolitical angst from Europe to Hong Kong has also intensified demand for havens, with the world’s pile of negative-yielding debt climbing to $17 trillion last week.

Still, not everyone sees yields falling further. Economists surveyed by Bloomberg in August had a median year-end forecast for the 10-year Treasury yield of about 2%, down from July’s prediction of 2.15%.

JPMorgan strategists led by Jay Barry in New York see the yield ending the year at 1.50%, close to current levels, though that’s down from their earlier prediction of 1.95%. They then see just a modest increase to 1.6% for the first half of 2020.

“Our forecast assumes only modest mean reversion into next year,” the strategists said. “The premium priced into Treasuries will not dissipate until there is evidence that global risks to the expansion are receding and that trade tensions are easing.”

--With assistance from Stephen Spratt and Sarah Ponczek.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, ;Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen, Nicholas Reynolds

©2019 Bloomberg L.P.