Japanification Stalks New Zealand Debt That’s 37% Owned by RBNZ

Japanification Stalks New Zealand Debt That’s 37% Owned by RBNZ

(Bloomberg) -- The Reserve Bank of New Zealand’s growing dominance of its bond market is sparking unfavorable comparisons with Japan.

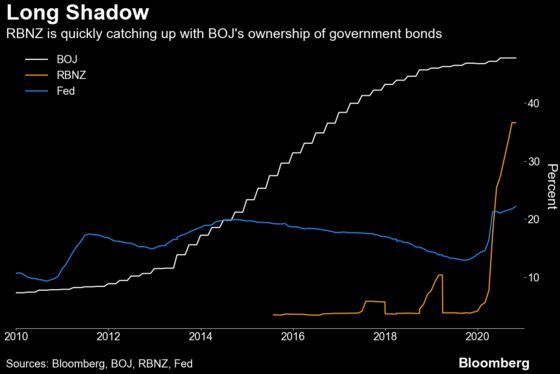

The RBNZ’s ownership of the nation’s outstanding nominal government bonds has rocketed from 6% to 37% in the space of seven months, according to calculations by Bloomberg based on data from the central bank. It took Bank of Japan Governor Haruhiko Kuroda more than three years to reach this level, and his starting point was over 11%.

The ultra-aggressive quantitative easing program has helped to cushion the New Zealand economy, but as was the case in Japan, it risks killing bond market volatility, sapping trading interest and crimping bank earnings. A subdued market with depressed yields may also deter overseas investors, limiting foreign capital needed to fund the current-account deficit.

“The RBNZ is really the ‘kiwi whale’ from a bonds and monetary policy perspective,” said Prashant Newnaha, senior rates strategist at TD Securities in Singapore. “The risk is they’ll crowd out other investors. Yields may get to a certain level where investors question whether there’s any point in buying the bonds at all.”

The developments Down Under underscore the challenges faced by central banks globally as they double down on stimulus that runs the risk of overwhelming bond markets. Unprecedented quantitative easing is prompting investors to take more risk for positive returns as about 26% of the world’s investment-grade debt now has yields below zero.

The market has yet to fully price in the risk of New Zealand’s debt becoming like Japan’s, according to Martin Whetton, head of fixed-income and currency strategy at Commonwealth Bank of Australia. But, the central bank’s huge presence is already on show.

Japan’s Shadow

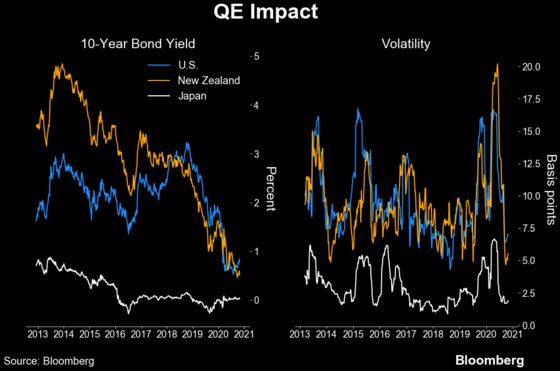

Volatility in the Japanese debt market has halved since the BOJ stepped up its quantitative easing in April 2013. Market liquidity has diminished by about one-third and the benchmark yield has dropped by half a percentage point. The BOJ owns about 48% of outstanding sovereign debt.

In New Zealand, volatility in 10-year notes has fallen by about two-thirds from a year ago, though it is still three times greater than that seen in Japan. Yields have dropped about 80 basis points during this period, putting them within about half a percentage point of the levels in Japan.

Although the RBNZ’s debt holdings are climbing steadily, it isn’t a given that it will maintain the current pace of purchases. And while the government agreed to raise the central bank’s cap on purchases of nominal bonds to 60% of the market, rising debt sales may keep it below this for the duration of its current program that’s targeting NZ$100 billion of bond purchases by June 2022.

Nick Smyth, a senior interest rates strategist at Bank of New Zealand, said it is “quite possible” that the market will have low yields and volatility for a long time but that liquidity is unlikely to be hurt.

“I think New Zealand is much less likely to be stuck in Japanification,” he said. “New Zealand is more likely to remain correlated with offshore yield moves, despite RBNZ QE.”

Smyth sees the RBNZ absorbing all the new net supply by June 2022 and the free float in the market remaining around where it was before the pandemic.

The BOJ shifted its focus in 2016 from a quantitative target to yield-curve control amid concern that it would run out of bonds to buy and as the low yields hurt the nation’s financial companies and returns on insurance products.

The coronavirus has also raised more questions over the European Central Bank’s hold over bond markets. Before, the institution was subject to strict restrictions on the proportion of a country’s debt it could buy in order to avoid accusations of debt monetization. Its more recent pandemic bond purchase program though isn’t subject to such restrictions, meaning that a growing share of the market will be dominated by the ECB.

Struggling Economy

In New Zealand the risk may be more that the RBNZ’s bond-buying program crowds out the foreign investors, who have been the biggest buyers of government bonds.

Of course, weaker global demand for New Zealand bonds may help contain any appreciation in the currency, which would support the central bank’s efforts to stoke inflation while lower yields revive economic growth.

This is crucial given that while New Zealand has succeeded in suppressing the coronavirus, border restrictions are likely to keep slowing the inflow of immigrants and decimate income from international tourism and education.

The steady inflow of students and immigrants has bolstered New Zealand’s economy and is a key point that differentiates it from Japan, said Toru Nishihama, an economist at Dai-ichi Life Research Institute Inc. in Tokyo.

“Should a prolonged slow recovery in the global economy from the pandemic change this assumption, there will be a risk that New Zealand’s bond market becomes like Japan’s,” he said.

©2020 Bloomberg L.P.