CLO Appetite in Japan Prompts Regulator’s Warning on Risk

Japan Warns Some CLOs May Not Be as Different as They Seem

(Bloomberg) -- Japan needs to remain vigilant about its banks’ overseas investments in bundled credit products because the underlying loans may be less spread out across industries or individual companies than they appear, a senior regulatory official said.

‘’Even if banks individually think they are well-diversified, it is possible that overall risks in the market are concentrated in the same sector or the same debtors,” said Tokio Morita, director-general of the Financial Services Agency’s Strategy Development and Management Bureau. “It is important for us to continue to analyze the situation closely” to prevent trouble for the financial system, he said.

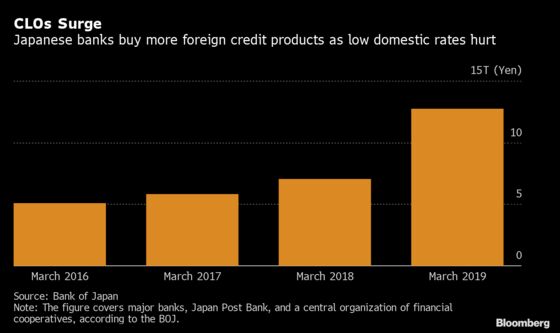

Financial regulators have been signaling caution about the rapid expansion of the collateralized loan obligation market, fearful that the products could be vulnerable to a downturn in the global economy. At a time of negative government bond yields at home, Japanese banks have been enthusiastic purchasers of U.S. and European CLOs, with agricultural lender Norinchukin Bank alone amassing 7.9 trillion yen ($72 billion) of the assets.

The Financial Stability Board, which acts as a global lookout for systemic risks in the banking system, said last week it encountered “important” data gaps in a study of exposure to leveraged loans and CLOs. That suggested threats to financial stability are hard to assess because of uncertainties as to who holds the debt.

The FSB report also noted the danger of concentration risk, pointing to a recent estimate that 90% of U.S. CLOs have exposure to at least one of the top 50 borrowers, and more than 80% are exposed to the top five debtors.

That’s an uncomfortable parallel with the implosion in the collateralized debt obligation market during the global financial crisis. CDOs were supposed to spread risk across a large portfolio of assets, but experienced a wave of cascading and correlated defaults after the housing crash.

Morita said it’s unlikely that Japanese banks will suffer large losses on their CLO holdings as long as they hold them to maturity. That’s partly because they have mostly limited their purchases to CLOs with high-credit ratings, he said.

However, the FSA is paying attention to whether the quality of the underlying loans is worsening and to whether their financial covenants are being relaxed, according to Morita. “We are also watchful of whether buyers will have the capacity to hold them to maturity if the markets move sharply,” he said.

While Japanese banks own 15% of outstanding global CLOs, almost all of them are rated AAA, according to a Bank of Japan report in October. Nevertheless, the report also warned that ratings and market prices of even top-rated CLOs “could fall substantially” if economic and market conditions change significantly.

Insurer Holdings

CLOs held by Japanese life insurers and brokerages are at ‘’not very worrisome” levels, Morita said. The FSB report said insurers represent the largest CLO holders after banks globally, and their holdings include lower-rated slices of the vehicles, meaning that ‘’stress episodes could therefore have negative implications” for them.

Japanese insurers held a relatively small amount of leveraged loans and $7.4 billion of CLOs as of December 2018, equivalent to about 0.2% of their assets under management, the FSB said. Roughly half or the CLOs are AAA-rated, it added.

Morita has been one of the leaders of fresh efforts by the FSA and the BOJ to strengthen collaboration to ward off potential financial crises, including a joint survey of Japanese firms’ CLO holdings earlier this year which informed the global FSB report. Other joint initiatives include testing banks’ resilience to risks including economic slowdowns, and polling financial firms on their preparedness for an anticipated phase-out of the Libor interest-rate benchmark.

Morita said he thinks the two authorities can work together in such areas as checking big Japanese banks’ ability to raise funds in foreign currencies, and studying the impact of rising corporate debt internationally.

“It now is important for us to start taking actual, collaborative actions with the Bank of Japan in a forward looking manner to deal with potential systemic problems,” he added.

The FSA has found no major issues so far in its regular checks on large banks’ foreign-currency funding, Morita said. “That said, market conditions could change -- we must keep thinking whether more can be done by banks to enhance” their fund raising abroad, he added.

Following the Bank of England’s initiative to assess the exposure of lenders and insurers to global warming, Morita said this is a “quite important” issue for the FSA as well. But at this stage the priority for Japan is to participate in global discussions on how financial authorities should get involved, he said.

To contact the reporters on this story: Takashi Nakamichi in Tokyo at tnakamichi1@bloomberg.net;Takako Taniguchi in Tokyo at ttaniguchi4@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Katrina Nicholas

©2019 Bloomberg L.P.