Japan’s 2025 Budget Goal Is Near Impossible, Debt Panel Member Says

Japan’s 2025 Budget Goal Is Near Impossible, Debt Panel Member Says

(Bloomberg) -- Japan’s target of balancing its budget by fiscal 2025 is essentially out of reach and pushing for it too hard would derail the pandemic-hit economy, according to Ayako Fujita, a member of the finance ministry’s debt-management panel.

“It’s pretty much impossible,” Fujita said of the goal to balance the government’s budget excluding debt-servicing payments by the year ending March 2026.

Measures such as spending cuts or tax increases to meet the goal would shave 1% off the economy each year and are therefore unlikely, Fujita, a senior economist at JPMorgan Securities, said in an interview.

The panelist’s remarks come amid continued insistence by Finance Minister Taro Aso that Japan is sticking with the goal. Aso reiterated his stance on April 30 that the goal is important to maintain market trust in the country’s commitment to fix its finances and to avoid a surge in yields.

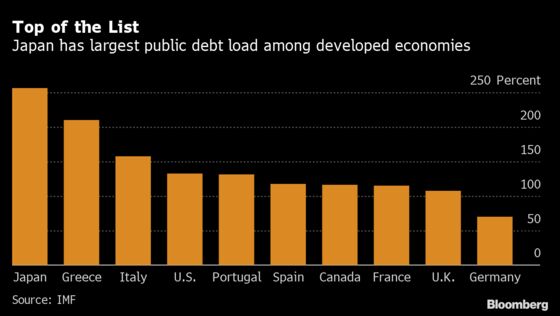

The International Monetary Fund’s latest estimate showed Japan’s public debt load compared against gross domestic product at 256%, the worst among developed nations. Even before the surge in government spending during the pandemic, Japan’s Cabinet Office forecast the country would fail to reach a primary balance this decade.

Read More: Covid-19 Pushes Japan’s Budget Balancing Further into Future

Still, once the economy has shrugged off the negative impact of the pandemic, the government should tackle the task of managing the nation’s growing debt, Fujita said.

To do that the government needs to start discussing how extra spending will be paid for and get back in step with the Bank of Japan on trying to generate inflation.

“Government policies such as reducing mobile phone fees or offering cut-price travel incentives are standing in the way of the BOJ’s efforts to spur inflation,” Fujita said. “The government should take measures to spark, not dampen, inflation, since it’s a significant factor in stable debt management.”

While the BOJ’s yield curve control policy aimed at generating stable inflation helps keep government borrowing costs down, it will eventually undermine debt management, she said. That will happen through deterioration in the functioning of the bond market needed for smooth issuance of debt and by lowering inflation expectations, she added.

| Fujita also said: |

|---|

|

©2021 Bloomberg L.P.