Italy’s Bond Sale Demand Thins Ahead of Risks From Draghi to ECB

Italy Plans Bond Sale Ahead of Market Risks From Draghi to ECB

(Bloomberg) -- Italy is locking in historically low financing costs at the start of a year where inflationary and political pressures could spell an end to super easy borrowing conditions.

Rome is selling seven billion euros ($7.9 billion) of new 30-year bonds via banks on Wednesday. The offering saw above 55 billion euros of orders, less than two thirds that for a similar sale in October 2020, showing demand for debt has faded compared to the height of the pandemic.

The country’s borrowing costs have already climbed around 30 basis points in the past two weeks on concerns that the European Central Bank may cut pandemic era stimulus and that Prime Minister Mario Draghi could step aside.

“We’re in a period of rising rates, with waning central bank support, and of political uncertainty with Draghi potentially calling it quits as PM,” said Antoine Bouvet, a rates strategist at ING Groep NV. “This may account for some reluctance to bid long-dated Italian bonds, even if they are a better option in my view than short-dated ones in case of heightened volatility.”

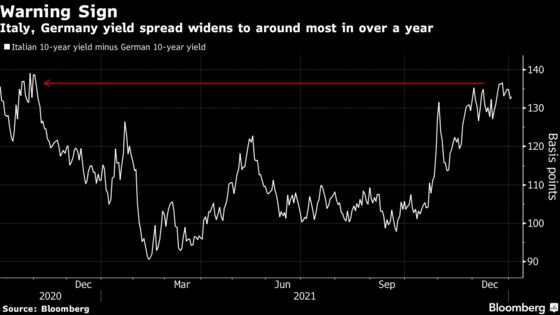

The premium investors demand to hold Italian debt over Germany -- a key bond market gauge of risk -- is near the highest since 2020. Other governments may look to follow Italy by frontloading bond sales, given major central banks from the Federal Reserve to the Reserve Bank of New Zealand are seen hiking interest rates this year.

The extra bond supply from Italy led its debt to underperform regional peers on Wednesday. In another sign that traders are making room for the sale, the yield premium between five- and 30-year bonds rose two basis points to 164 basis points, the highest since November.

Long-end bonds are also under pressure given the prospect of monetary tightening. ECB officials have struck a hawkish tone on inflation risks after confirming last month that they would wind down a pandemic bond-buying program. Italian bonds have been one of the biggest winners from the central bank’s support, and also benefited from the stabilizing force of Draghi’s leadership last year.

Draghi, whose political support in Italy’s coalition government is waning, has hinted he might agree to become the country’s president if parliament votes to select him in a process due to start on Jan. 24. If he switches role, that would cut short the government’s term and could spark an early general election.

The election of Draghi to president would trigger “a new period of political instability for Italy,” said Christopher Dembik, head of macro analysis at Saxo Bank. “The Italian presidential election is not on investors’ radar yet, but expect a hard awakening and market turmoil and bond volatility in the BTP market in case of snap elections.”

Italy mandated Barclays Plc, BNP Paribas SA, Deutsche Bank AG, Intesa Sanpaolo SpA and JPMorgan Chase & Co. for the sale. The pricing was set at six basis points above comparable bonds, tightening two basis points from initial guidance. The amount offered was slightly below the expectations of Commerzbank AG’s 8 billion-euro forecast.

©2022 Bloomberg L.P.