Italy Is Racing to Keep Debt Costs Lower for Longer

Italy Is Racing to Keep Debt Costs Lower for Longer While It Can

(Bloomberg) -- Italy is seizing on the torrent of stimulus in Europe to push its mountain of debt payments further into the future.

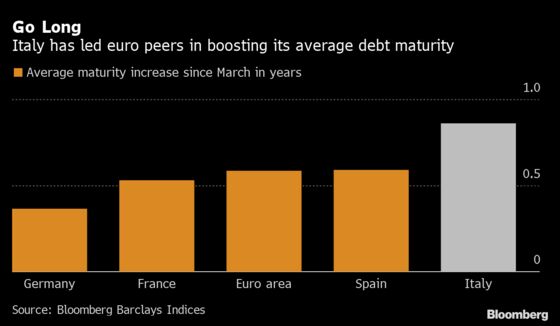

Since the onset of the pandemic in March, the nation’s Treasury has extended the maturity on its debt stock by about a year, the most among major peers in the euro area, and 40% more than the average for the region, according to Bloomberg Barclays indexes.

That will knock 300 million euros ($364 million) off Italy’s financing bill this year, according to Morgan Stanley strategist Tony Small. When the added windfall from the European Union’s recovery fund and social bond sales are taken into account, he estimates the Treasury could save as much as 10 billion euros in 2021.

The government sits on one of the largest debt loads as a percentage of output in the euro area, yet the average maturity on these liabilities is the lowest among the bloc’s biggest economies, a problem compounded by the level of government borrowing now needed to combat the pandemic. Domestic political wrangling and clashes with the EU over national budgets have given way to costly bursts of market volatility over the past decade.

The ECB’s bond-buying response this year has provided a golden opportunity for debt management offices to sell bonds over longer periods and for a cheaper rate, putting even the shakiest of government finances in the region on a more solid footing. Italy has been buying back short-dated notes and exchanging them for new longer-dated securities, spreading out the burden on its obligations.

“This means that debt-to-GDP ratios which are above 100% will be sustainable,” said Jolien van den Ende, a strategist at ABN Amro Bank NV, who recommends investors position for Italian bonds to extend a rally. She expects the spread on 10-year securities over their German equivalents -- a key gauge of risk in the region -- will narrow to 80 basis points, a level last seen a decade ago.

Morgan Stanley, meanwhile, estimates that Italy’s debt servicing costs will fall to the lowest level since the euro’s inception in 1999 within the next two years, even as it piles on more borrowing. The country has sold over 100 billion euros more of longer-maturity bonds this year than originally planned, Italy’s Director General for Public Debt Davide Iacovoni said last month.

Golden Opportunity

Thanks to the European Central Bank’s bond buying program, demand has been plentiful. By far the best performing sector this year has been debt maturing beyond the 20-year mark, with money managers clamoring for returns moving further along the curve to pick up yield.

There are signs that other member states are also taking advantage of this voracious investor appetite. The Netherlands and Belgium have both upped their issuance of long-dated bonds, Spain sold two 50-year notes this year and Austria added another century bond to its portfolio.

This might all be a moot point given the ECB expanded its bond-buying armory Thursday. Commerzbank AG expects the central bank will purchase more than Italy’s entire net supply of debt next year. Still, the nation’s strategy of pushing out the maturity on its bond portfolio has merits, even if the ECB is a buyer of last resort.

“It lowers the refinancing risks, as there will be a smaller amount to refinance,” said Jan von Gerich, chief strategist at Nordea Bank ABP. “It also takes advantage of the historically low long bond yields, and with that provides more certainty that borrowing costs will be low in the future as well.”

“Market conditions for Italy in particular have not always been that favorable to issue in long maturities,” he said. “Now they are.”

Bank of England

The Bank of England meets to set policy on Thursday. Investors are bringing forward expectations for more easing, as the prospect of the U.K. leaving the EU without a trade deal at the end of the year increases.

Money-market traders are now pricing in a 10-basis-point interest-rate cut to 0% by August, from December 2021 previously, and a further five basis-points reduction by the end of next year.

Next Week

- Euro-area and U.K. bond issuance has concluded for the year and debt management offices are gradually publishing next year’s plans

- Italy pays 12.9 billion euros on the redemption of a floating-rate note next week

- The BOE will buy back 4.4 billion pounds of debt across three operations next week

- Data releases have been pushed forward ahead of year-end with preliminary manufacturing and services PMI for December for the euro area, Germany and the U.K. as well as France, all due on Wednesday; Germany’s Ifo survey for December will be released on Friday

- November inflation, retail sales and October earnings, unemployment numbers are due in the U.K.

- Investors will hope to glean clues on monetary policy from ECB’s Pablo Hernandez de Cos and Olli Rehn who speak next week

- BOE’s Ben Broadbent speaks on Thursday following the rate decision

- There are no major sovereign ratings reviews scheduled for the euro area or U.K. until next year

©2020 Bloomberg L.P.