Italy Contagion Fears Bubbling Beneath Surface of Apparent Calm

Italy Contagion Fears Bubbling Beneath Surface of Apparent Calm

(Bloomberg) -- The latest collision between Italy’s markets and politics is beginning to fuel concern that shock waves could spread to elsewhere in Europe.

As Italian bond yields touched a four-year high, the euro extended losses and the region’s equities slumped, while haven assets such as German bunds and the Swiss franc rallied. Goldman Sachs Group Inc. warned that the risk of a wider impact of the Italian turmoil has increased, even as markets in Spain and Portugal -- seen as a key barometer for any debt contagion to Europe’s periphery -- have so far shown little sign of anxiety.

Budget official Claudio Borghi’s comments that the common currency is “not sufficient” to solve the country’s fiscal problems have rekindled worries that a breakup of the world’s largest trade bloc is still a possibility. He later denied that the country’s populist government had any plans to leave the euro. Two-year German debt, a popular hedge against regional risks, saw smaller gains this week than in May, suggesting that the latest Italian sell-off is driven more by concern about fiscal weakness than the risk of an exit from the euro.

“European risky assets remain vulnerable and there is potential for negative spillovers to the euro area given the high trade exposure to Italy,” Goldman Sachs strategists led by Alessio Rizzi wrote in a research note. “While our economists do not expect systemic implications for the global economy, contagion risks have risen.”

Markets were firmly in risk-off mode Tuesday, with demand rising for popular risk hedges. Italy’s two-year bonds took the brunt of the selling pressure, flattening the country’s yield curve. The cost of protection against a potential credit default by the nation rose and traders priced in a greater premium for three-month money-market borrowings over overnight loans.

Euro, Yields

The euro dropped by as much as 0.6 percent Tuesday to $1.1505, a six-week low. Italian 10-year yields climbed 15 basis points to 3.45 percent, the highest since March 2014. The spread over those on their German peers breached 300 basis points for the second time this year.

Still, there’s little sign yet of a contagion effect across peripheral euro-area bonds. Ten-year yields in Spain and Portugal were little changed at 1.54 percent and 1.90 percent, respectively. Similar rates in Greece climbed nine basis points to 4.31 percent.

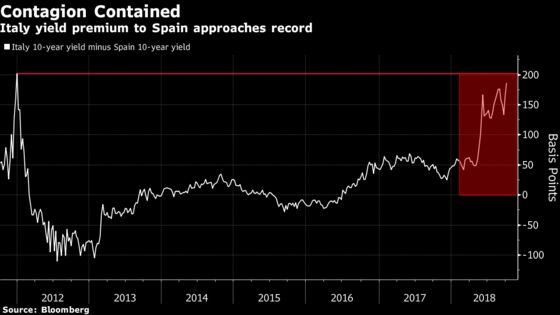

The yield premium investors demand on benchmark Italian bonds over Spain has hit a seven-year high and is climbing toward a record 202 basis points reached in 2011. Strategists at Banco Bilbao Vizcaya Argentaria SA including Jaime Costero expect the spread to widen further, as Spanish debt retains its appeal amid little spillover impact from Italy’s market volatility.

‘Local’ Issue

“Political developments in Italy are still center-stage and will probably continue to remain the most critical driver for the euro for the time being,” analysts at UniCredit SpA wrote in a note. “Still, contained contagion in the bond markets implies that the budget talks are still perceived as a “local” issue. The market behavior suggests to us that the Italian developments are likely to just add “noise” to the common currency at the moment, but are not seen as grave enough to trigger a heavy sell-off.”

Strategists at Credit Agricole SA led by Valentin Marinov remain bullish on the euro as they see most of the Italy-related negativity already priced in, and with continued support from the European Central Bank’s monetary-policy normalization. Even as Italy’s bonds and stocks saw increased volatility in recent months as the country’s Five Star Movement-League coalition drew up their deficit targets, the shared currency had been relatively resilient.

‘Fade the Pop’

The Italian economy’s underlying strength may mean it’s time to ease out of risk-off hedges despite political risks, according to Mizuho International Plc.

“The protection trades are ramping up,” head of European rates strategy Peter Chatwell said. But “this is a great opportunity for investors to fade the pop in some structures. Most obvious, to us, is to fade the rally in German bonds outright, as we do not think this flare-up between Italy and the EU will drag on the euro-area economy.”

For others, Italy’s euroskeptic government is just the embodiment of the the populist sentiment taking root across Europe, which could threaten the bloc’s future and weigh on the euro for the months or even years to come.

Borghi, head of Italy’s lower house budget committee and a well-known euroskeptic, said in an interview on Radio Anch’io that “Italy, with its own currency, would be able to resolve its problems.”

“The comments about Italy having its own currency have touched a sore point,” said Jane Foley, head of foreign-exchange strategy at Rabobank International. “While the return of the lira would be almost impossible and hugely inflationary even if it could happen, the fact that the remarks can be read as anti-EMU sentiment are worrisome.”

--With assistance from James Hirai.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma

©2018 Bloomberg L.P.