Italy Bonds Fail to Lure $2 Trillion Investors After Budget Deal

Italy Bonds Fail to Lure $2 Trillion Investors After Budget Deal

(Bloomberg) -- Some of the world’s biggest bond investors are shunning Italy’s debt even though its government solved a budget dispute with the European Union.

AllianceBernstein, Aberdeen Standard Investments and AXA Investment Managers, which between them oversee over $2 trillion, are resisting the temptation to buy some of the highest-yielding government securities in the euro area. Money managers remain skeptical they will be compensated enough for risks including the prospect of a recession, elections or a banking crisis.

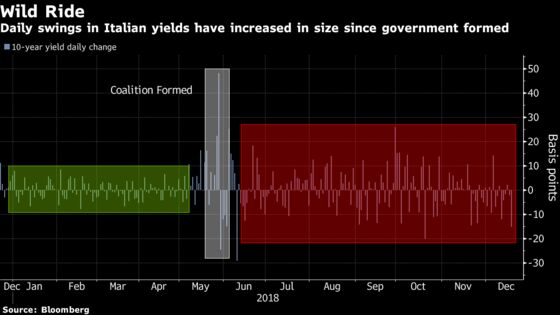

That reluctance has led them to miss out on a recovery in the debt in recent weeks, capped by a rally on Wednesday after the populist government secured a deal to avoid EU penalties over its spending plans. The months-long standoff with the bloc had roiled the country’s bond and stock markets.

“It’s getting harder to remain with my basic starting point of ‘don’t buy Italy,’ for sure,” said Aberdeen money manager Luke Hickmore, who maintains an underweight position on the debt. “But expect an election, prepare for a recession and worry about bank funding liquidity.”

Italy’s benchmark yields are heading toward the end of the year at about 2.80 percent, 80 basis points higher than they started 2018. The yield spread over German debt has fallen back to about 255 basis points, still above the level before the government first proposed a higher deficit in September.

Risks Persist

The battle with the EU has served to expose tensions between the coalition’s partners -- the Five Star Movement and the League -- and their spending priorities. While the former is in favor of a citizen’s income for the poorest, the latter is trying to cut taxes. The new deficit plan could widen the rift to raise the prospect of fresh elections in the new year.

For AllianceBernstein money manager John Taylor, Italian corporate bonds look more attractive than sovereign bonds based on expected returns. He could, however, renew long positions in government bonds should a more market-friendly administration emerge next year.

“The lower deficit target next year may well lead to a new election, which the market will view as positive if it changes the coalition from the current mix to one which involves a more mainstream party,” he said.

The prospect of a deep economic slowdown is likely to take over as the main source of concern for investors now that the budget problems have been put to one side. Barclays Plc and Bloomberg Economics expect a contraction in the fourth quarter, which would tip the country back into recession.

“The market has anticipated well the political resolution of the Brussels-Rome clash, but we need to break below 2.5 percent to suck in more buyers, and volatility needs to collapse,” said AXA chief investment officer Alessandro Tentori. “Long-term issues of potential growth persist and won’t be resolved by fiscal policy.”

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, Keith Jenkins

©2018 Bloomberg L.P.