Repo Squeeze Threatens to Spill Over Into Funding Markets

Repo Squeeze Threatens To Spill Over Into Funding Markets

(Bloomberg) -- What started out as a funding shortage in a key U.S. money market is now making it more costly to get hold of dollars globally.

A sudden surge in the overnight rate on Treasury repurchase agreements that began on Monday continued Tuesday -- with the rate opening at 7%, according to ICAP.

Although technical factors that have dumped more collateral into the repo market and siphoned cash out are likely the cause, the squeeze has raised the specter that the Federal Reserve may be struggling to control money-market rates. For long-time Fed watcher Lou Crandall of Wrightson ICAP, the dislocations are so worrisome that he says the Fed may for the first time in a decade this morning do its first overnight system repo to deal with the funding squeeze.

“There is a significant risk” that the federal funds rate -- the Fed’s target for which is its key policy tool -- will on Tuesday exceed the 2.25% upper end of the central bank’s range, Wrightson analysts wrote in a note dated Tuesday.

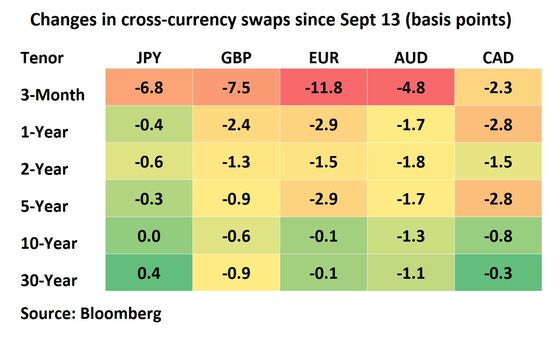

This is all filtering into a demand for dollars that is already showing up in swap rates from euros, pounds, yen and even Australia’s currency. As an example, the cost to borrow dollars for one week in FX markets while lending euros almost doubled.

The squeeze may be short-lived -- with analysts pointing to a confluence of two factors for a sudden shortage of dollars -- but it still highlights the vulnerability of a key borrowing market.

What happened was an unfortunate coincidence -- just as companies were withdrawing cash from money markets to pay corporate tax, a glut of new bonds appeared on the market as the U.S. government sold some $78 billion of 10- and 30-year debt last week.

With just $24 billion of bonds maturing in the period, this became one of three occasions this year when the imbalance between debt redemption and cash needed to buy new Treasuries exceeded $50 billion.

Suddenly there was a scarcity of dollars at the same time as a glut of Treasuries, which banks typically lend out to investors with spare cash through repurchase agreement. As a result, the overnight repo rate more than doubled to 4.75%, the highest level since December, according to ICAP pricing.

“Repo pressure is almost entirely a settlement story with $54 billion of net supply in Treasury coupons landing on already very crowded dealer balance sheets,” Blake Gwinn, head of front-end rates at NatWest Markets, wrote in a research note. The tax deadline probably exacerbated the situation, he wrote.

The increase in repo rates then pushed up the cost of holding Treasuries, leading the spread between two-year yields and interest-rate swaps to shrink on Monday.

It wasn’t long after that that dollar-funding stress started showing up elsewhere, with the three-month premiums to swap currencies such as euros or yen into dollars jumping. Short-dated eurodollar futures dropped, and implied rates rose, as short-term funding rates climbed.

Bigger Problems

The repo market remains vulnerable to short-term liquidity squeezes anyway due to structural issues, which often surface around year-end.

“The culprit is the scarcity of bank reserves, which are the only asset that provides banks with intraday liquidity,” Priya Misra, head of global rates strategy at TD Securities in New York, wrote in a note. “Reserves have been declining since 2014 and we expect them to decline further as Treasury’s cash balance increases and currency in circulation grows.”

--With assistance from Alexandra Harris, Joanna Ossinger and Liz Capo McCormick.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, ;Benjamin Purvis at bpurvis@bloomberg.net, Nicholas Reynolds

©2019 Bloomberg L.P.