Brave New World of ESG Bonds Can Sometimes Leave Investors Cold

Investors Worry About Profiting From Bonds That Miss Green Goals

(Bloomberg) -- A new type of bond that penalizes issuers for failing to meet social and environmental goals is raising concern among some investors that buying the debt may not be all that ethical.

Japanese real estate firm Hulic Co. recently joined a handful of borrowers worldwide in selling so-called sustainability-linked bonds, but the market’s reception has been underwhelming. Such securities offer an extra coupon if the issuer fails to meet goals, and for some investors that raises a troubling question: is it really ethical to profit from a company missing its green or social targets?

The muted reaction is fueling an early debate about whether the booming market for environmental, social and governance (ESG) investments risks skewing incentives for issuers. There have also been broader concerns that the cutting-edge laboratory of ESG bond design sometimes churns out structures that have design flaws. Many investors have struggled with other structures, for example, to figure out what’s really green and what’s “greenwashing” -- the use of misleading labels to create an undeserved image of environmental responsibility.

Hulic barely sold out its 10 billion yen ($96 million) of 0.44% notes last month, at a time when orders for other green bonds in Japan have far exceeded the supply.

Globally only about 10 issuers including Chanel Ceres Plc and Novartis AG have sold sustainability-linked securities after the world’s first such issuance last year from Italian utility Enel SpA.

“If the issuer achieves its goal, a low coupon can be treated as a reward for them, which makes sense,” said Nao Kobayashi, deputy manager of the investment department at Mitsui Sumitomo Insurance Co. “But if it fails, a step-up coupon is considered as a penalty, and it doesn’t sound right for us to benefit from someone’s penalty.”

The insurer decided not to buy Hulic’s bonds because the coupon was low for a 10-year security with an A+ credit rating, Kobayashi said. While her firm is interested in new ESG products, it probably would continue to avoid notes that profit investors when issuers miss targets, she said.

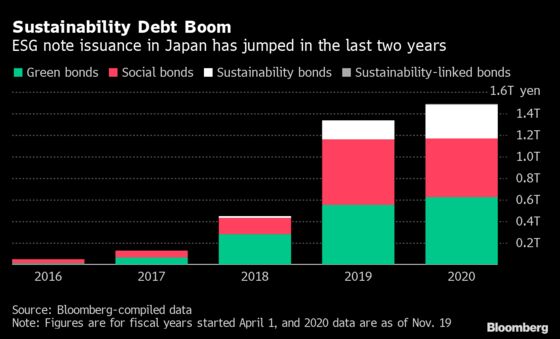

So far, global issuance of such securities has totaled $11.8 billion worldwide, a fraction of the $1.1 trillion outstanding of environmental, social and governance bonds, according to Bloomberg-compiled data.

There has also often been discussion in the market about the way ESG-focused investors could hesitate to buy sustainability-linked securities, given the structure with the coupons stepping up if the goals aren’t met, according to Atul Jhavar, head of APAC green & sustainable capital markets at Barclays Bank Plc.

But there are signs that offerings may expand ahead, after the International Capital Market Association published guidelines for the securities in June. HSBC Holdings Plc has said sales may boom next year, after the European Central Bank said it will start buying such notes in January.

See also: Sustainability-Linked Bond Sales to Boom Next Year, HSBC Says

Investors in Hulic’s debt get 10 extra basis points on the coupon if the company fails to meet environmental goals. Orders for the notes came to 1.1 times the amount issued. That compared with 1.5 times for 10-year green bonds sold by Sumitomo Warehouse Co. and two times for similar-maturity green securities issued by Tohoku Electric Power Co., according to underwriter data.

The Hulic bond “shows our commitment that we strive to achieve our goals,” said Yoshihiro Yamada, a company spokesman. “The purpose of the sales is to expand the investor base to those who want to invest in our company in the mid to long term.”

©2020 Bloomberg L.P.