Investors Torn Between Following Fed or Trusting Bond Traders

Investors Torn Between Following Fed or Trusting Bond Traders

(Bloomberg) -- When it comes to interest rates, Federal Reserve Chairman Jerome Powell has said that “an ounce of prevention is worth a pound of cure.” Bond investors may be better off backing traders’ calls for a pound upfront.

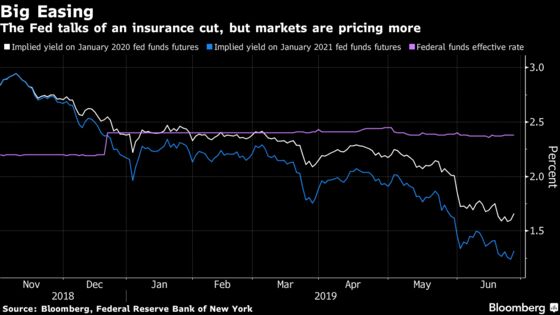

After all, traders have been right pretty much all year, as their rate-cut bets have kept them a few steps ahead of the Fed as it’s tilted more dovishly. The central bank now looks poised to ease, but even one of its arch doves, St. Louis Fed President James Bullard -- the only voter to dissent this month in favor of lower rates -- says more than a quarter-point move in July would be “overdone.”

Traders aren’t really buying the case for a modest tweak. They’re pricing in almost 100 basis points of cuts in the next 12 months, in what’s starting to resemble an easing cycle for an economic downturn. That leaves investors with a tough decision: put their faith in the rates market’s pessimistic outlook and risk missing out on a record-breaking expansion; or trust the Fed’s signaling and risk being caught wrong-footed if the economy slumps.

The Fed’s message is, “We can tweak and things will go back to normal,” said Bret Barker, a portfolio manager at TCW Group, which oversees $165 billion in fixed-income assets. “That usually makes our hair stand up a little bit.”

Barker is on alert for the prospect of deeper cuts. He’s positioning for the yield curve to steepen, led by falling front-end yields.

That’s already happening. The two-year yield has dropped about 75 basis points since March to 1.74%, touching the lowest level since November 2017. That’s about 27 basis points below the 10-year yield, close to the widest gap this year.

Looking Up

Jim Caron at Morgan Stanley Investment Management is in a more optimistic camp toward the economy. He’s eyeing inflation-linked bonds on the view that lower borrowing costs could lift inflation expectations, which still imply price pressures running well below the Fed’s target over the next decade.

“We don’t really think that there’ll be a material yield fall from here,” said Caron, whose firm manages $480 billion. While a further slide in the 10-year rate is possible, he doesn’t see it getting below 1.75%. His portfolios are slightly long Treasuries, but he’s considering moving to a more neutral footing.

He could be leaning the wrong way if TD Securities proves right. Global head of rates strategy Priya Misra sees yields falling further, and is penciling in 150 basis points of Fed cuts by the end of next year. TD sees scope for record-low 10-year yields should the Fed cut multiple times.

“The Fed will certainly spin the first cut as insurance,” Misra wrote in an email. “I’m really not convinced that a couple of rate cuts will help manufacturing or business investment and sentiment improve.”

Big Moment

Of course, the weightiest issue in the market right now is what happens with U.S.-China trade relations. Investors who are undecided on whether to put their money on the Fed or the rates market may find the scales tipped this weekend.

The scheduled meeting between the leaders of the world’s two largest economies isn’t expected to resolve what’s likely to be protracted negotiations. But a “non-negative” outcome, as MSIM’s Caron describes his base case for the encounter, may give investors more confidence in the Fed’s vision.

--With assistance from Liz Capo McCormick and Christopher Condon.

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Elizabeth Stanton

©2019 Bloomberg L.P.