Investors Deserve a Peek at Bond Managers’ Tricks

Investors Deserve a Peek at Bond Managers’ Tricks

(Bloomberg Opinion) -- Active bond managers have dazzled investors by outpacing the bond market in recent years. But it’s a simple sleight of hand, and the big reveal is coming.

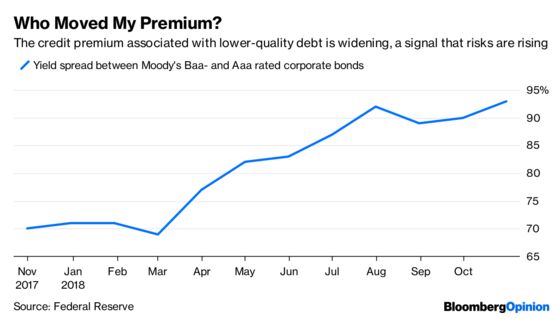

The trick is that bond managers have been quietly loading up on low-quality bonds. They pay a higher yield than top-quality ones to compensate for their greater risk of default — in technical parlance, a credit premium.

When times are good, as they have been in recent years, there are few defaults because borrowers have little trouble paying their debts. Bond managers collect their credit premiums and easily beat the broad bond market indexes, which tend to be dominated by high-quality bonds.

When the economy slows, however, the defaults start to pile up, handing losses to holders of low-quality debt. And suddenly bond managers don’t look so smart.

It’s a worthwhile trade-off for managers. The booms normally last longer than the busts, which means that credit premiums are usually a boost to performance. And nothing attracts investors like a hot hand, or the appearance of one.

But it’s not great for investors. They often don’t realize that their bond manager is taking more risk until the losses show up. And investors who want riskier bonds can almost always buy them more cheaply through index funds. They would be better served by a closer inspection of bond managers’ tricks of the trade.

All of this is poised to spill into view. According to my Bloomberg Intelligence colleague Eric Balchunas, only 7 percent of active bond managers have beaten the Bloomberg Barclays U.S. Aggregate Bond Index in the past month, a widely used gauge of the broad bond market.

The culprit is those low-quality bonds. I counted 788 actively managed bond mutual funds, including their various share classes, that are benchmarked to the aggregate bond index and have a track record of at least three years. Their average duration, or sensitivity to changes in interest rates, is similar to the index, according to Morningstar data. The big difference is credit quality. The average rating of the bonds they hold is BBB, far lower than the index’s average rating of AA+.

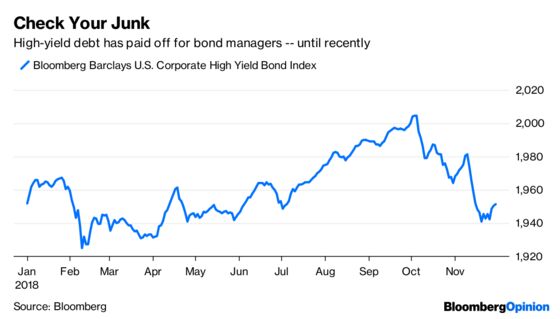

While credit risk has paid off in recent years, it’s beginning to bite. The funds have beaten the aggregate bond index by an average of 0.68 percentage points a year over the last three years, a substantial margin for bond managers. But over the last month, they’ve fallen behind by an average of 0.63 percentage points.

There are reasons to worry that more pain is coming. The prices of lower-quality bonds are still rich despite recent declines. Some companies have also taken on too much debt. Federal Reserve Chairman Jerome Powell rightly observed last week that “highly leveraged borrowers would surely face distress if the economy turned down, leading investors to take higher-than-expected losses.” And there are signs that the U.S. leveraged-loan market is stumbling.

There’s an easy way to give investors more visibility into their bond funds: Grade managers using benchmarks that more closely resemble their investing styles. For example, the Bloomberg Barclays U.S. Fixed Income Balanced Risk Index has a similar duration as the aggregate bond index, but more credit risk. Its average credit rating is A-, which is closer to the average credit risk of the actively managed bond funds I looked at.

Not surprisingly, when those funds are compared with the balanced risk index, much of their outperformance — and recent underperformance — evaporates. The funds beat the index by an average of 0.25 percentage points a year over the last three years and trailed by 0.39 percentage points over the last month. An index with an average credit rating of BBB would even more closely track the funds’ performance.

Bond managers will resist changes to their scorecard, and not only because their performance would be less flattering. They undoubtedly see what’s happening to stock pickers and are eager to avoid their fate.

Actively managed stock funds were once compared with the broad market, too. But then came indexes that better track managers’ styles, initially value and growth, small and large cap, and more recently momentum, quality and others. Soon afterward, low-cost mutual funds and exchange-traded funds began tracking those indexes, making it nearly impossible for stock pickers to beat them. Investors are increasingly pivoting to the index funds.

The same trend is already unfolding in bond investing. A BlackRock ETF tracks the balanced risk index with an expense ratio of 0.25 percent, a fraction of the average expense ratio of 0.88 percent for the bond funds.

And there are others. The Bloomberg Barclays Enhanced U.S. Aggregate Bond Index weights bonds based on yield rather than market capitalization, so it also has more credit risk than the aggregate bond index. And the Bloomberg Barclays U.S. Universal Index throws in some international bonds. There are low-cost funds that track both indexes.

Bond investors may not be paying much attention now, but they will when managers’ bets on credit turn south. And when that happens, a new generation of bond funds will come into view.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2018 Bloomberg L.P.