To Sniff Out Insider Trading, Follow the Options Market

To Sniff Out Insider Trading, Follow the Options Market

(Bloomberg Opinion) -- Insider trading involves illegal profiting from nonpublic information by people buying and selling shares. It typically increases whenever companies are busy acquiring each other. The 42 percent rise in the Russell 3000 index during the 24 months through September included the most mergers and acquisitions in 12 years. Now the technology that created artificial intelligence is getting good at detecting stock market fluctuations that can only be explained as abnormal, sophisticated and nefarious.

Bloomberg algorithms give market participants help identifying unusual activity in stock, bond, currency and derivatives trading. The automated analysis of derivatives like options can also expose otherwise opaque insider trading activity that was once evident only with the fluctuations of the underlying assets of bonds, commodities, currencies and equities.

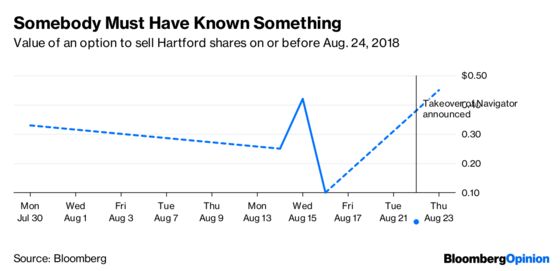

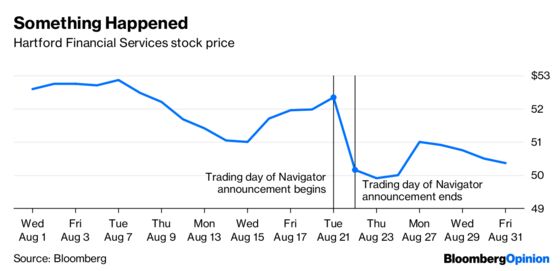

For example, the Bloomberg algorithm provides fresh insight into suspiciously opportunistic trading around a takeover deal last summer. During the month preceding Hartford Financial Services Group Inc.’s Aug. 22 agreement to buy Navigators Group Inc. for $70 a share, there is no public record that such a deal was in the works. But people anticipating the $2.1 billion acquisition prepared to triple their money on Aug. 14 by betting that Hartford would plummet on the news a week later. We know there was a likelihood of insider trading because the volume of Hartford options rose more than four times the 20-day average for that period eight days before the announcement, according to data compiled by Bloomberg.

While Hartford’s shares were unchanged at $51.41 on Aug. 14, the options market was exploding with puts and calls. Puts give holders the right, but not the obligation, to sell shares at a specified price on or before a specified time. Calls give holders the right with no obligation to buy shares at a certain price on or before a certain date.

When Bloomberg News reported, “Hartford Financial Option Volume Up, Led by Aug. 24, $50.50 Puts” on Aug. 14, the information was surprising because the put-call volume ratio of 67 was almost 18 times the average during the past year. In other words, for every one call purchased, there were almost 67 puts purchased. Such unusual activity confirmed that investors were especially eager to sell Hartford stock — overwhelming negative sentiment when the stock market was otherwise quiescent. Bloomberg News reported a similar surge in bearish option bets on Aug. 16.

When the purchase of Navigator was disclosed six days later, Hartford shares fell 4.2 percent — a decline that had occurred as steeply only eight times during the past four years, according to data compiled by Bloomberg.

On Aug. 16, the value of the suddenly popular Hartford puts increased more than four times to 45 cents from 10 cents, providing a profit of $3.5 million for every $1 million used to buy the Hartford puts. Navigator shares, meanwhile, rallied 12.6 percent, the biggest seven-day increase since at least 2001, without any news suggesting a higher stock price was justified. The people who turned bullish on Aug. 8 stood to make at least 20 percent, or $200,000 for every $1 million invested, according to data compiled by Bloomberg.

The Hartford-Navigator deal was no isolated example of suspicious activity as the stock market approached record highs during the summer, the Bloomberg algorithms show. A day before Diamondback Energy Inc. said it was acquiring Energen Corp. for $9.2 billion in an all stock transaction, Bloomberg reported, “Diamondback Implied Volatility Surges,” which is another way of saying that trading in Diamondback options rose to more than six times the 20-day average for the period, and that people were preparing to profit on an unforeseen event. Diamondback’s shares fell as much as 13.8 percent on the news of its acquisition, the biggest intraday decline in the company’s history, according to Bloomberg data.

That was only half the equation. Twenty-five minutes before the deal was announced on Aug. 14, Bloomberg News reported, “Energen Option Volume Jumps, Led by Oct. 19, 2018 $80 Calls.” Trading in Energen options rose four times the 20-day average for the period. With hardly anybody wanting to sell, the put-call volume ratio sank to 0.002 compared with an average of 1.42 during the past year. In other words, people were suddenly making big bets that Energen was about to rally. By Aug. 20, the value of the popular Energen calls more than tripled to $3.50 from $1.05, enabling the people who purchased them to make a profit of almost $2 million for every $1 million invested in the derivatives, according to Bloomberg data.

Another case in which people appeared to be profiting from nonpublic information surfaced a month before Reuters said on July 11 that Apollo Global Management LLC approached Nexstar Media Group. Bloomberg’s June 11 report, “Nexstar Media Option Volume Surges, Led by June 15, $70 Calls,” revealed that trading in Nexstar options climbed to 18 times the 20-day average at that point. The put-call ratio of 0.01 suddenly collapsed from the 1.21 average during the past year, which could only be interpreted as an overwhelming bet that Nexstar was poised to rally. Sure enough, after Nexstar calls doubled to $2.6 on June 11, they appreciated 232 percent four days later, allowing holders to net $2.3 million for each $1 million used to exercise the calls, according to data compiled by Bloomberg.

These suspicious recent bursts of puts and calls look a lot like some of the illegal activity that occurred during a merger boom in the last bull market, before the 2008 financial crisis. That’s when Bloomberg reported in May 1, 2007 that trading in options to buy shares of Dow Jones & Co. surged to an 18-month high before News Corp. announced its $5 billion bid for the company that day. But the news report followed the News Corp. announcement and was based solely on an old-fashioned survey of data without the help of any algorithms.

Ten months later, former Dow Jones & Co. director David Li and three other Hong Kong residents agreed to pay more than $24 million to settle a U.S. probe into alleged insider trading before the News Corp. takeover.

(With assistance from Shin Pei)

To contact the editor responsible for this story: Jonathan Landman at jlandman4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is a Bloomberg Opinion columnist. He is the editor-in-chief emeritus of Bloomberg News.

©2018 Bloomberg L.P.