Inflation Not Deficits Is the New Challenge for Pakistan’s Economy

Inflation Not Deficits Is the New Challenge for Pakistan’s Economy

(Bloomberg) -- High inflation is emerging as the new challenge for Pakistan, where authorities are trying to secure an International Monetary Fund bailout to avert a balance-of-payments crisis.

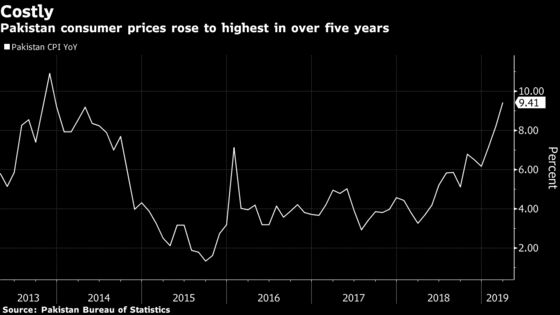

Consumer prices in March rose to the highest level since 2013, with gains seen hovering above 8 percent through the first-quarter of 2020. That is likely to put the State Bank of Pakistan, the most aggressive central bank in Asia, on course to tightening monetary policy further, according to Yousaf Hussain, chief executive officer at Faysal Bank Ltd.

Inflation “is nearing the peak,” Hussain said in an interview. There may be a 50 to 100 basis points increase in key interest rate “in the short run.”

The central bank has raised rates by a cumulative 475 basis points since last year as it sought to contain the financial blowouts from Pakistan’s twin current-account and budget deficits, which limited the nation’s ability to retire debt and pay for much-needed imports.

While concerns about current-account gap have abated for now, inflation is way above the central bank’s average forecast range of 6.5 percent to 7.5 percent for the year ending June. That’s an added worry for a nation, whose credit score was downgraded by S&P Global Ratings citing a worsening economic outlook amid a delay in striking a deal with the IMF.

An IMF team is expected to visit Islamabad for discussions at the end of the month as Prime Minister Imran Khan promised structural reforms.

“With the IMF coming in, you follow a very regimented approach that gives a lot of confidence to foreign investors, they can see some certainty in the direction the economy is following,’’ said Hussain.

To contact the reporter on this story: Faseeh Mangi in Karachi at fmangi@bloomberg.net

To contact the editors responsible for this story: Arijit Ghosh at aghosh@bloomberg.net, Karthikeyan Sundaram, Abhay Singh

©2019 Bloomberg L.P.