Infamous ‘No-Coupon-At-All’ Club May Soon Welcome Another Member

Infamous ‘No-Coupon-At-All’ Club May Soon Welcome Another Member

(Bloomberg) -- It’s one of the bond market’s most dubious honors, a mark of shame that among even the very worst deals in history, few carry.

Dubbed ‘no-coupon-at-all,’ it’s reserved to describe securities that default before making a single payout. The distinction is so rare that it’s generated a cult-like following among traders, who recall just a handful of transactions in recent decades that fit the bill.

But now, they’re on alert for another potential entry into the infamous club. Hertz Global Holdings Inc. last week issued a so-called going concern warning, telling creditors it may be forced to file for bankruptcy amid dim prospects for a rapid recovery in its travel-dependent car rental business. That would leave its $900 million of 6% notes sold back in November in default before paying investors a dime.

“I wouldn’t be surprised if there are many more” to come, said George Schultze, founder and CEO of Schultze Asset Management, which specializes in distressed and special-situations investing. “The fixed-income market is so speculative, investors will fund anything.”

A representative for Hertz declined to comment.

It’s not as if these bonds were destined for the trash heap since the day they priced. The Estero, Florida-based company was originally looking to raise $750 million before getting enough investors interest to increase the size of the deal. The unsecured notes were rated B3 by Moody’s Investors Service and B- by S&P Global Ratings, well into junk territory but hardly unique.

Somewhat rarer, they carried an issuer recovery rating of 6 from S&P, the lowest rank, meaning lenders can expect between 0% to 10% of their principal back in the event of a payment default.

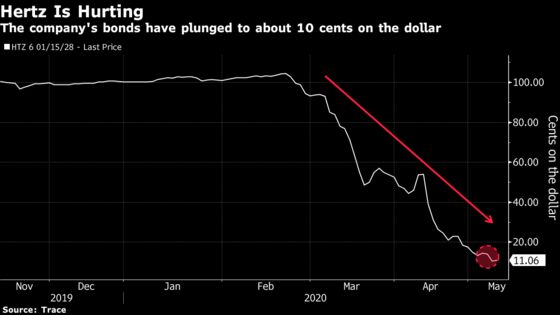

That’s sure to be weighing on the securities, which are trading at just 11 cents on the dollar, according to Trace.

With the company facing a Friday deadline to pay other creditors about $400 million, market watchers may find out sooner rather than later whether the ignoble ranks of the no-coupon-at-all club are set to swell.

In the meantime, here are some of the most notorious members in recent memory.

MF Global

MF Global Holdings Ltd., the holding company for the broker-dealer run by ex-Goldman Sachs Group Inc. co-chairman Jon Corzine, sold investment-grade bonds in August 2011 that promised to pay extra interest if Corzine departed for a position with the Obama administration. He didn’t. Instead, ill-timed bets on European government bonds led to MF Global’s swift descent into bankruptcy roughly three months later.

AmeriServe Food Distribution

AmeriServe Food Distribution Inc. was one of the nation’s largest distributors to fast-food chains including Pizza Hut and Taco Bell before it filed for Chapter 11 bankruptcy in January 2000. But three months earlier, AmeriServe arranged a $200 million junk-bond sale. Investors sued the underwriter and claimed they were misled, as the company apparently was having difficulty with its suppliers and customers for months. AmeriServe never paid its first coupon, and eventually all the assets were liquidated.

Just For Feet

One of the largest athletic-shoe retailers at the time, Just For Feet Inc. sold $200 million of 11% senior notes at par in April 1999. They were used to repay an $80 million term loan and a portion of the company’s revolver. But bondholders never got a dime of interest as sales slowed and stores were quickly shuttered. Less than a year after the notes were issued, Just For Feet filed for bankruptcy with a pre-negotiated plan in place, which gave creditors common stock in the reorganized company to cut its debt load in half.

©2020 Bloomberg L.P.