The Bond Market’s $1 Trillion Deficit Spiral Has No Political Fix

The Bond Market’s $1 Trillion Deficit Spiral Has No Political Fix

(Bloomberg) -- Democrats and Republicans have plenty at stake in the upcoming midterm elections. But it’s already looking like a no-win situation for the U.S. bond market.

If Democrats take the House, it raises the odds that congressional leaders will propose an infrastructure-spending bill similar in scope to President Donald Trump’s original trillion-dollar proposal. And if the GOP defies expectations and holds on in Congress, tax cut 2.0 becomes more likely. In either case, the result will be debt, debt and more debt.

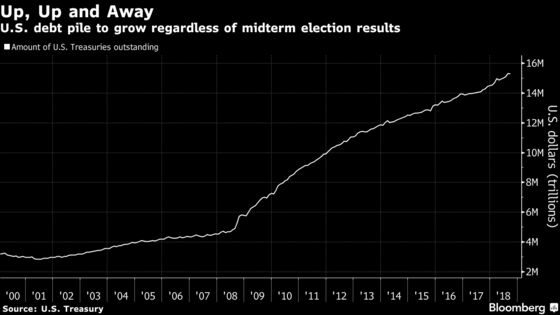

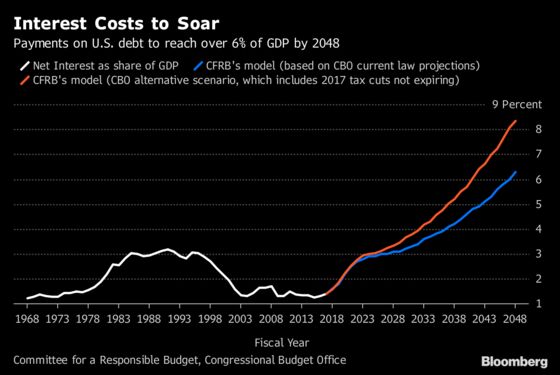

That’d be on top of what is already a grim fiscal situation. A deluge of debt supply is set to inundate the $15.3 trillion Treasury market, just as borrowing costs rise. Not only is the U.S. budget deficit primed to swell to roughly $1 trillion by fiscal 2019 and past that in subsequent years, but the interest owed by the government is also forecast to triple in the coming decade to nearly a trillion dollars a year, according to the Congressional Budget Office.

“The current debt trajectory is already quite onerous,” said Subadra Rajappa, an interest-rate strategist at Societe Generale. “If you keep increasing supply and auction sizes, there is a point where the bond market is going to say, ‘Thanks, but no thanks.’”

The consequences could be far-ranging. With Treasury Secretary Steven Mnuchin set to double new issuance this year and the Federal Reserve scaling back its debt purchases, any dropoff in investor demand for the burgeoning supply of U.S. Treasuries could mean tens of billions of dollars in additional interest -- all of which taxpayers would ultimately have to pay. Starting today, the Treasury Department will auction $230 billion of debt, ranging from one-month bills to 30-year bonds this week.

Signs of pushback have already started to appear. At varying times this year, a strong economy, a hawkish Federal Reserve and worries about the deficit and inflation have all conspired to sour investors on Treasuries.

In recent weeks, the yearlong selloff in Treasuries has accelerated, pushing yields -- the effective cost for the U.S. government to borrow money -- to multiyear highs. Last week, the 10-year note soared above 3.2 percent for the first time since 2011. Demand at a recent Treasury debt auction (where the U.S. actually borrows the money it needs) also fell to a decade low.

Of course, it’s perfectly reasonable to think that Democrats will have zero appetite to do Trump any political favors before the next presidential election cycle, like passing an ambitious infrastructure spending bill. And Republicans may suddenly re-discover that they’re supposed to be the party of fiscal discipline and hold the line on more tax giveaways.

Debt Burden

But even if nothing changes on Capitol Hill, America’s finances are far from secure.

Trump’s once-in-a-generation tax cut, along with increased spending for Social Security and Medicare as the baby boomer generation retires, are already set to boost the public debt burden by $10 trillion over the next decade, CBO estimates show. By that time, net interest costs will reach $915 billion. (That’s up from a record $523 billion in interest paid in the year ended Sept. 30.)

The risk is that spiraling debt will prompt investors to drive up borrowing costs, à la the “bond vigilantes” of the 1990s Clinton era. The CBO already sees 10-year yields at nearly 4 percent by 2020. They’re currently at 3.23 percent. Following the central bank’s policy meeting last month, Fed chairman Jerome Powell said “we’ve been on an unsustainable fiscal path.”

“In the end, we will have to face that,” he said.

Regardless of who wins, Bob Miller, the head of U.S. multi-sector fixed income at BlackRock, says the fund giant expects that, excluding T-bills, the Treasury Department will issue almost three times as much debt next year on a net basis as it did in 2017, when it sold roughly $400 billion of notes and bonds.

Deficit Spending

It’s not hard to see how the U.S. could end up even deeper into the red.

Based on polling, fundraising and historical trends, Democrats have a good shot at gaining the 23 seats they’d need to take control of the House. Republicans are expected to keep the Senate, where they currently hold a narrow majority. Former economic adviser Gary Cohn said last month he wouldn’t be surprised if a Democratic House majority comes out of the gate with a fully debt-financed infrastructure plan -- and Trump signs off on it. (The Trump administration’s plan favored a mix of public and private investment.)

“If the Democrats win the House I will be shocked if the first thing they don’t do is infrastructure,” he said. “Another trillion dollars of debt, here we come.”

Thomas Simons, an economist at Jefferies, predicts Democrats and Trump could agree to spending measures that add $150 billion in net debt annually. The firm expects 10-year yields to reach 4.3 percent by the end of 2019.

Worst-Case Scenario

“If you split the legislature, that means you need more buying-in from different parties,” said Jason Schenker, president of Prestige Economics and author of ‘Midterm Economics.’ “The way you do that is usually more allocated government spending and debt.”

Even worse for bond investors, however, would be if Republicans hold onto both houses of Congress, says Dana Peterson, an economist at Citigroup. That would embolden the GOP to try and make its tax cuts permanent. (The current law, which Trump signed in December, will expire for individuals after 2025.)

“Ten years from now, you will have a really outsized deficit and a lot of debt,” Peterson said. So if the tax changes become permanent, “the market will price in those expectations now.”

Whatever the case, Jefferies’ Simons says what’s clear is that there’s going be a lot more debt on the horizon, and it’s going to get more costly.

“Here’s a certainty: It doesn’t matter who wins, we’re going to be issuing debt forever,” Simons said. “There will be a push toward more expansionary fiscal policy. Be ready.”

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Michael Tsang, Larry Reibstein

©2018 Bloomberg L.P.