If U.S. Intervenes in FX, Even Dollar Bears Say to Buy the Dip

If U.S. Intervenes in FX, Even Dollar Bears Say to Buy the Dip

(Bloomberg) -- Here’s one thing dollar bulls and bears can agree on: In the unlikely event that the U.S. intervenes to weaken its currency, it’d be a good time to buy.

President Donald Trump said Friday that he hasn’t ruled out taking action to cheapen the greenback, and that a strong dollar makes it “harder to compete.” His comments followed weeks of speculation among analysts about the possibility of U.S. intervention amid the president’s repeated complaints about other countries’ currency practices.

However, the administration would likely face an uphill battle trying to influence the foreign-exchange market, which trades about $5 trillion daily. The Treasury’s Exchange Stabilization Fund holds almost $23 billion in greenbacks and around $50 billion in special drawing rights that it could convert, and the Federal Reserve has been an equal participant in the last three U.S. currency interventions. While intervention is unlikely, the resulting “limited” dollar declines would likely entice traders, according to State Street Global Advisors.

“The market’s going to be willing to fight against that and really challenge the Fed and Treasury,” said State Street Global senior portfolio manager Aaron Hurd, whose group manages $125 billion. While he’s bearish on the greenback, “I’d be looking to buy dollars if that’s the case.”

Wild Card

The U.S. last intervened in FX markets in 2011, along with international peers, after the yen soared in the wake of that year’s devastating earthquake in Japan. That effort buoyed the dollar. However, analysts have been contemplating the wild-card notion that the U.S. could forcibly weaken the dollar. It hasn’t taken that step since 2000, also as part of a coordinated move, to buoy a tumbling euro.

Unilateral action by the U.S. would diminish intervention’s effectiveness, wrote Pacific Investment Management Co.’s Gene Frieda and Tiffany Wilding in a blog post Monday. The U.S. is unlikely to gain international cooperation to “competitively devalue” the dollar in the current environment of global trade friction, they wrote.

“Without the blessing of global peers, intervention would increase uncertainty, and the negative consequences for global growth would outweigh any benefits to the U.S. from a softer dollar,” they wrote.

Bigger Stockpile

Stephen Jen and Joana Freire of hedge fund Eurizon SLJ estimate that the Treasury would need closer to $350 billion in its ESF to muscle the dollar lower. However, a solo foray would likely prompt retaliation from other countries, they wrote in a note to clients this month.

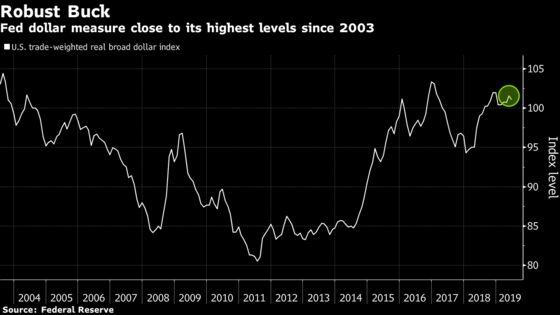

Trump has grown concerned that the U.S. currency’s strength will undermine his economic agenda. A Fed trade-weighted measure of the dollar that adjusts for inflation isn’t far below its highest since 2003.

The dollar’s haven status would give traders another reason to buy an intervention-triggered dip, according to Krishna Memani, Invesco Advisers vice chairman of investments. Investors would likely seek shelter in American assets as trade tensions would escalate, he said.

“If the U.S. does unilateral currency intervention to get the dollar lower, effectively the markets will see that as another form of the trade war,” said Memani. “We’ll get into risk-off mode and people will be piling into dollars.”

While Memani sees slim odds of U.S. intervention, “with Trump, you can never be sure.”

Then there’s the world’s roughly $13 trillion pile of negative-yielding bonds to consider. U.S. dollar sales would likely just create a buying opportunity in positive-yielding Treasuries, said former Treasury official Brad Setser. He’s now a senior fellow at the Council on Foreign Relations.

“If the U.S. succeeds in pushing the dollar down temporarily, in a sense it’s just making the yield that U.S. bonds offer available to foreign investors at a temporary bargain,” he said.

--With assistance from Anchalee Worrachate.

To contact the reporter on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Nick Baker

©2019 Bloomberg L.P.