If Fed’s ‘50 B’s’ Are Wrong Now, Then When Is Right?

If Fed’s ‘50 B’s’ Are Wrong Now, Then When Is Right?

(Bloomberg Opinion) -- In between tweets about Michael Flynn’s court appearance and Twitter making it hard for him to accumulate followers, President Donald Trump on Tuesday made an eye-catching remark about monetary policy: “Stop with the 50 B’s,” he told the Federal Reserve.

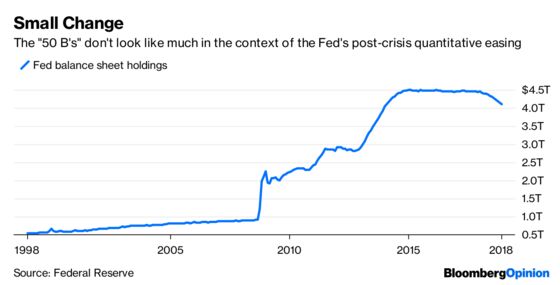

For those who don’t understand the reference, Trump was referring to the Fed’s policy of trimming its balance sheet by up to $50 billion a month. To do so, policy makers let their current holdings of U.S. Treasuries and mortgage securities mature without reinvesting the proceeds. Since it began in earnest in October 2017, the central bank’s bond portfolio has dropped to about $4.1 trillion, from as much as $4.5 trillion four years ago. Before the financial crisis, it held less than $1 trillion.

The balance sheet ballooned, of course, because of the Fed’s unprecedented quantitative easing. An editorial in the Wall Street Journal, which Trump encouraged central bankers to read, built off commentary from Stanley Druckenmiller and Kevin Warsh, who posited that because the bond-buying program raised the prices of risk assets, like U.S. stocks, a reversal would naturally send the markets downward, as they have for much of the past few months.

When it comes to the future path of interest-rate increases, Fed officials may very well be content with raising this week and then holding off for months. But this slow and steady balance-sheet reduction will almost certainly continue for at least another year or two, for one simple reason: If not now, when?

The U.S. economy is strong. The unemployment rate, at 3.7 percent, is the lowest since 1969. Wages are growing at close to the fastest pace since 2009. Inflation is right around the Fed’s 2 percent target. Yes, some data are starting to weaken, but from elevated levels in the first place. What happened to celebrating second-quarter economic growth of more than 4 percent?

Active investors used to bemoan the lack of volatility in markets because of the Fed’s heavy hand, which boosted asset prices indiscriminately across the board. Now that the central bank is ever so slightly scaling back, they’re crying foul again. Shouldn’t this be the time that market savants like Druckenmiller shine? The Fed’s job isn’t to support risk assets by whatever means necessary; rather, it’s specifically designed to try to deflate areas of excess.

To Fed Chairman Jerome Powell’s credit, he understands this, which is why his standard response to questions about the balance sheet is that he wants to let holdings continue to roll off in the background, with changes to the fed funds rate serving as the central bank’s primary monetary policy tool. Of course, if markets are to be believed, he may no longer have that option available. Traders are pricing in one increase, at best, in 2019.

The amount is sometimes less than that, however, because the Fed doesn't have enough Treasuries and mortgage-backed securities maturing to meet or exceed the monthly cap.

Ben Hunt, or @EpsilonTheory on Twitter, drew a similar conclusionin response to the WSJ op-ed.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.