High-Yield Debt Market Momentum to Roll Into 2021

High-Yield Debt Market Momentum to Roll Into 2021

(Bloomberg) -- An uptick in M&A activity, alongside an economic recovery, as well as fiscal and monetary stimulus should keep the European sub-investment grade market running hot in 2021.

The arrival of Covid-19 vaccines has boosted investor confidence, and helped support the rally in bonds of companies still battered by lockdowns. An effective roll-out of the vaccine -- as well as a surge in M&A -- should clarify which firms survive next year.

“Next year you will clearly see who are the winners and losers,” said Sander Bus, co-head of credit at Dutch money manager Robeco Institutional Asset Management.

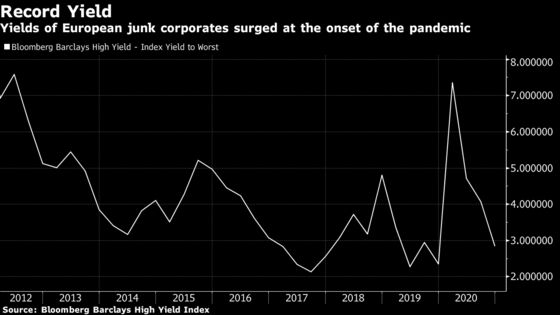

Junk issuers’ popularity increased in 2020 amid investors hunt for yield. In Europe, the European Central Bank’s and the Bank of England’s bond-buying programs pushed investment grade investors into buying riskier paper. While that trend may continue for the short-term, monetary and fiscal support won’t last indefinitely.

“When the economy is in transition, it’s always problematic for credit,” Bus said. “Unlike what happens with equities, you’re always capped at par on the upside, but you’re exposed to losses.”

Any delays to vaccination programs and structural changes, such as homeworking, will require industries to adapt. Regardless of the help at hand, many companies are unlikely to make it through next year.

Read More: European High-Yield Defaults to Hit 8% as Support Fades: S&P

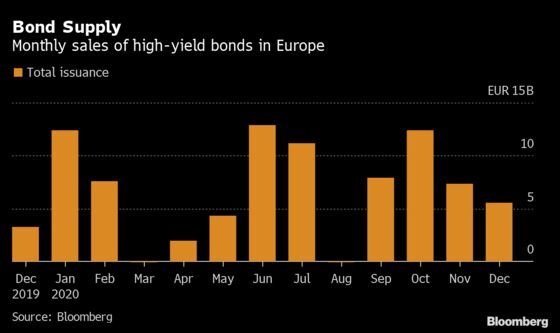

Issuance

European high-yield primary market is set to close this year with a volume of issuance around 86 billion euros ($104.6 billion), the most since 2017. That’s despite the eight-week hiatus between March and April and the traditional August break.

The trend was supported by companies tapping the market to bolster their liquidity, some large pre-pandemic M&A transactions, such as Thyssenkrupp AG’s sale of its elevators unit, the downgrade of investment-grade companies, and at the end of the year, refinancings.

Next year is likely to feature more M&A-driven deals.

“The pipeline is already building for bond-financed acquisitions,” said Andrew Hagan, partner at lawfirm Freshfields Bruckhaus Deringer LLP.

Daniel Rudnicki Schlumberger, head of EMEA leveraged finance origination at JPMorgan Chase & Co, sees firms that have emerged relatively unscathed from the crisis as poised to take advantage.

“We expect to see M&A in sectors more affected by Covid, where companies that have performed better will buy competitors to consolidate sectors, or companies more affected by the pandemic will start selling assets,” he said.

Refinancings and amendments to some challenged capital structures will also help in primary activity, Schlumberger added.

Stimulus Dependency

The monetary and fiscal stimulus, such as government-backed loans and furlough schemes, have supported the economy and look set to keep doing so in 2021.

ECB’s Bond-Buying Plan Pushes Investors to Riskier End of Market

Debt looks cheap these days because of low interest rates, but this could change if the central banks withdraw their support earlier than expected. Likewise, the end or reduction of the fiscal stimulus programs in place would mean a blow for many overlevered companies.

“Now people don’t care about the debt figure, but it could be like in 2008-2011,” said Per Wehrmann, head of European high-yield at DWS Investment GmbH. “Two-three years after the financial crisis, investors saw the risks of sovereign debt and that could suddenly lead to more volatility in the likes of Italy or Spain.”

“Things are not as rosy as valuations would suggest,” said Andrey Kuznetsov, senior credit portfolio manager at Federated Hermes, who expects 2021 to be a relatively volatile year.

“We’ve had quite significant compression in the market,” he said. “I think the tighter we go, the easier it will be for us to respond quite materially to any leaked news that are considered at this point low-probability events by the market, like for example earlier than expected withdrawal of central bank support.”

The restrictions arising from reduced monetary support “could be the playbook of 2018, when we had the tapering by the Fed,” said Sunita Kara, a portfolio manager at Aviva Investors Global Services Ltd.

“This is one of the risks that we are keeping in the front of our minds when we think about the late stage of next year.”

©2020 Bloomberg L.P.