High-Yield Bonds Party Like There’s No Tomorrow

High-Yield Bonds Party Like There’s No Tomorrow

(Bloomberg Opinion) -- Bond traders are dusting off their tried and true post-crisis playbook after the Federal Reserve’s pivot last month. What they don’t realize is that the game has most likely changed.

In an unabashed reach for yield, investors suddenly can’t get enough of the riskiest debt, with the Bloomberg Barclays U.S. Corporate High Yield Bond Index posting a staggering 5.25 percent total return in the first five weeks of 2019, led by those securities rated in the CCC tier. In the largest CCC borrowing since September, Clear Channel Outdoor Holdings Inc. received orders this week of more than $5 billion for a $2.2 billion deal, allowing it to price its debt to yield 9.25 percent, compared with whisper talk of about 10 percent. CommScope Finance LLC boosted the size of its junk-bond offering to $3.75 billion from $3 billion because of strong demand.

December seems like forever ago. Remember, it was the first month in a decade that no speculative-grade borrower tapped the market. And even buoyed by no new issuance, junk bonds still fell the most in three years.

The recent rebound in high yield is hardly a surprise, given Fed Chairman Jerome Powell’s abrupt shift toward pausing on further interest-rate increases for a while. It’s the classic “risk on” market, apparently backstopped by the central bank, that investors have seen time and again in the almost 10 years since the last recession ended. The bigger fear seems to be missing out on this quick recovery: U.S. high-yield funds experienced $3.86 billion of inflows in the week ended Feb. 6, the biggest since July 2016, Lipper data show. It follows a flurry of Wall Street strategists rushing to increase their 2019 total return estimates for junk bonds just weeks into the year.

Bond investors are either looking for short-term profits with this frenzy or are oblivious to longer-term risks. As Andrew McCormick, head of fixed income at T. Rowe Price, put it in an interview: “If you’re going to buy risk, you want to be a renter rather than an owner.”

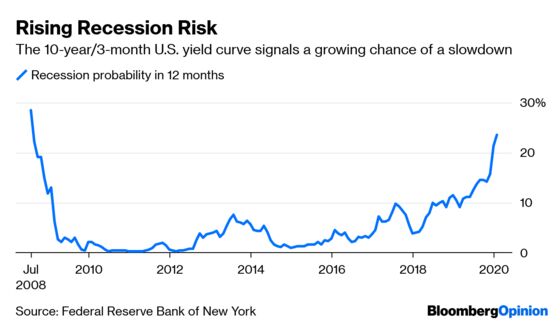

Consider the odds of a downturn, which is most detrimental to riskier borrowers. According to a model from the New York Fed, the probability of a U.S. recession in 12 months has climbed to almost 25 percent, the highest since 2008 and more than double what it was a year ago. Moody’s Investors Service has said slower growth this year will push the corporate default rate to 3.4 percent from 2.8 percent in 2018. Citigroup Inc. projects an even higher 4.6 percent default rate in 2019. That isn’t exactly a rosy outlook for speculative-grade issuers.

On top of that, the Fed’s Senior Loan Officers Survey released this week showed banks rapidly tightened lending standards for commercial and industrial loans. It’s usually a leading indicator for U.S. growth, as Bloomberg News’s Tracy Alloway noted, raising the question of whether the economy is just facing another blip or something bigger. Meanwhile, banks including Barclays Plc, Deutsche Bank AG, UBS Group AG and Wells Fargo & Co. are still trying to offload some leveraged-loan deals they were stuck with late last year.

That once-hot leveraged loan market, by the way, hasn’t come close to the blistering pace of the junk-bond rally, perhaps because investors prefer fixed-rate debt now that the Fed is on hold. In fact, individuals have pulled money from the funds for 12 consecutive weeks, including some of the biggest outflows ever.

So, what’s going on with high yield? Maybe it’s simple: “In typical market fashion, sentiment overshoots,” Robert Almeida, global investment strategist at Massachusetts Financial Services Co., said in an interview.

Even though it seems as if the prevailing sentiment is that the run in junk bonds can’t last, few seem willing to step in and say the rally is about done. The average spread on junk bonds is 4 percentage points, according to Bloomberg Barclays data. While that’s down from more than 5 percentage points at the start the year, it’s still far wider than October, when it was 3.03 percentage points. If investors really believe they’re “all clear,” there’s room for a further rebound.

Ultimately, though, the nearly 10-year U.S. expansion will slow, if not flip into a recession. To borrow McCormick’s phrasing, it’s a matter of how long investors are willing to “rent” junk bonds and reap the high interest payments before getting out.

As is the case with many strategies, that will work until it doesn’t. Again, it was less than two months ago that high-yield debt tumbled day after day, with volume in the biggest junk-bond exchange-traded fund eventually soaring to an all-time high during the height of the sell-off. And in October, the idea was floated that high yield could be a shelter during the equity-market storm. That proved not to be the case.

It’s understandable that investors are almost giddy that the Powell Fed seems to have their back (or, at least not making a perceived policy error). And it’s easy to simply equate “dovish Fed” with “risk on.” But don’t be fooled — pitfalls abound, particularly if buyers become indiscriminate in their reach for yield. They say markets have a short memory: Junk-bond buyers are proving it.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.