High-Tax States’ Bonds Are So in Demand That Ratings Don’t Matter

High-Tax States’ Bonds Are So in Demand That Ratings Don’t Matter

(Bloomberg) -- There’s so much money chasing after the bonds sold by America’s high-tax states that buyers don’t seem to care too much about what credit-rating companies think.

The heavy demand overall has driven municipal yields to their lowest in more than six-decades. And with rates so low, the yield penalties that would typically differentiate a deeply indebted state from a thrifty one have become little more than rounding errors that in some cases contrast with their standing in the ratings pecking order.

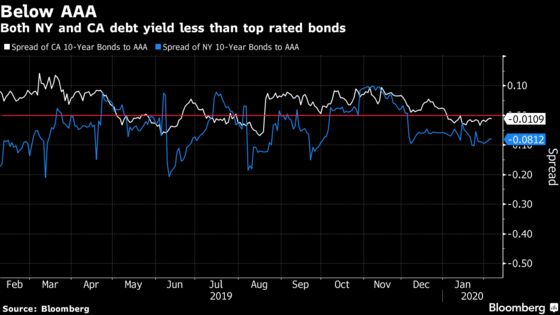

California’s general-obligation debt, for example, is yielding about 1 basis points less than the AAA benchmark, even though the state is rated as many as four steps below that, according to data compiled by Bloomberg. New York, one step below AAA, is paying about 8 basis points less than top-rated borrowers. Over the past year, New Jersey’s yield premium has been cut nearly in half even though its rating hasn’t changed. Connecticut’s is roughly a third of what it was.

By contrast, bonds issued by AAA rated Texas and Florida, where there’s no state income tax, pay above-benchmark yields.

This dynamic shows how dramatic the demand has become for tax-exempt securities since President Donald Trump’s 2017 tax law limited state and local deductions. That change drove investors in high tax-states like California, New York and New Jersey into municipal bonds as an alternative way to drive down what they owe.

“To boil it down, it’s 99.999% because of the SALT cap,” said James Iselin, portfolio manager at Neuberger Berman Group LLC in New York. “Because there’s is so much demand in the market -- there is less of a credit differentiation that the market is making.”

To contact the reporter on this story: Danielle Moran in New York at dmoran21@bloomberg.net

To contact the editors responsible for this story: Elizabeth Campbell at ecampbell14@bloomberg.net, William Selway, Michael B. Marois

©2020 Bloomberg L.P.