Italy Is Just One Reason Bunds Will Weather Treasuries Tumult

Here's Why the Treasury Drop Is Unlikely to Spell Doom for Bunds

(Bloomberg) -- Investors inclined to sell Treasuries without batting an eyelid are unlikely to repeat the feat on German Bunds.

While 10-year Treasuries have had the worst start to a month since March last year, Bunds haven’t exactly been rocked by volatility. German notes are being shielded by a host of factors, not the least of which are the European Central Bank’s reluctance to raise borrowing costs, political risks looming large over Europe and a currency-adjusted yield that compares favorably with U.S. bonds.

“The probability of the ECB failing to have a normal tightening cycle remains high,” Steven Major, global head of fixed-income research at HSBC Holdings Plc, wrote in a note to clients. “Forward guidance dictates that it is unlikely policy rates will be hiked before next summer and then there are three potential exogenous disruptors: Italy, Brexit and the U.S. rate cycle.”

Major expects the Bund yield to end 2019 at 0.50 percent, lower than its current level of about 0.55 percent.

Here are the reasons why German bond yields are likely to stay capped:

Diverging Policy

The extra yield that U.S. Treasuries offer over Bunds has been widening to new historic highs almost every day this month as the Federal Reserve continues to raise rates, while the ECB is set to sit on its hands until at least September next year. Any decline in Bunds stemming from the sell-off in Treasuries is unlikely to persist, according to many investors. In fact, Citigroup Inc. sees German yields at 0.65-0.70 percent as a buying opportunity, while NatWest Markets expects the gap between U.S. yields and Bunds to grow.

We are “short fixed income globally, but in places that are hiking and you have the central bank on your side,” NatWest strategist Jim McCormick wrote in a note to clients. “Should we be surprised by 4 percent U.S. 10s and 0.5 percent German 10s? No.”

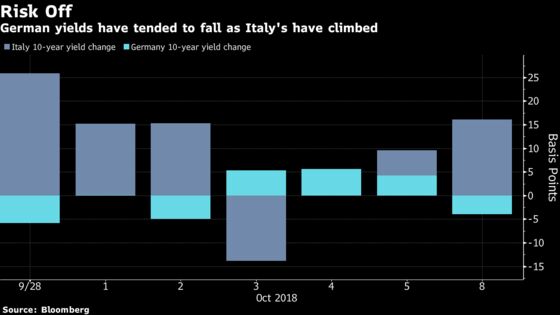

Italian Risk

Investors are also likely to seek safety in Bunds if the political ructions between Italy and the EU over the country’s budget take a turn for the worse and the U.K. exits the bloc without a deal in hand.

Italy’s proposed budget deficit of 2.4 percent of gross domestic product will do little to close country’s gaping debt load next year. The current stock is running above 130 percent of the nation’s economic output, prompting the EU to come down firmly on the Five Star Movement-League coalition.

German bonds have typically rallied as Italy’s have fallen. Mizuho International Plc estimates that Bunds would be trading 15 basis points higher than now, if the 10-year yield spread versus Italy was at 250 basis points, compared with over 300 currently.

Currency Play

Bunds look particularly attractive to investors based in the U.S if the cost of currency hedging is anything to go by. When protected against exchange-rate swings, German bonds offer a pickup of 50 basis points versus Treasuries, while Italian 10-year securities offer adjusted yields of nearly 7 percent.

That’s mainly due to a weaker euro, which may struggle to appreciate against the dollar as the the U.S. economy continues to outperform and Italy risk weighs.

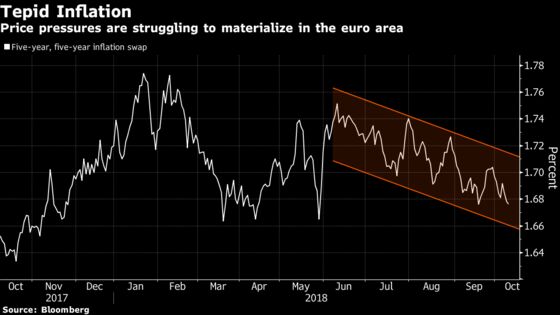

Cool Inflation

Despite a pickup in global growth and energy prices, domestic cost pressures are still lagging in the euro area, contributing to a deceleration in inflation to 0.9 percent in September from 1 percent a month earlier. Expectations for further out are also diminishing, with the five-year, five-year inflation swap rate sliding to the lowest in almost four months.

Not only does that complicate the picture for the ECB’s planned tightening, but also means yields don’t have to rise by as much anytime soon. Executive Board member Benoit Coeure said last week that “a bit of time” was needed for inflation to stabilize sustainably.

“This soothes such worries that the ECB is about to ‘do a U.S.’,” wrote NatWest’s Andrew Roberts.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Scott Hamilton

©2018 Bloomberg L.P.