Here’s What Market Strategists Are Watching in U.S. Job Data

Here’s What Market Strategists Are Watching for in U.S. Job Data

(Bloomberg) -- Friday’s U.S. June jobs report could prove significant for markets as the Federal Reserve gauges whether to cut interest rates for the first time in more than a decade.

One quirk of this jobs report: It comes on a summer Friday after the U.S. Independence Day holiday July 4, so market activity could dissipate quickly after the numbers come out if trading desks have less staffing than usual. The median forecast is for a nonfarm payroll (NFP) gain of 160,000 after a soft 75,000 in May. Average hourly earnings are seen rising 0.3% on the month after a 0.2% climb in May.

Here’s a roundup of views:

Hannah Anderson, global market strategist at JPMorgan Asset Management in Hong Kong

- Expects a gain between 100,000 and 200,000. About 150,000 “doesn’t necessarily spell forthcoming aggressive policy easing.”

- “If we get an employment report that’s as weak as last month’s, it makes it more likely they’ll cut sooner rather than later.”

- Second-quarter GDP in late July will likely be more critical for the Fed’s month-end decision than payrolls.

Shane Oliver, chief economist at AMP Capital Investors Ltd. in Sydney:

- “Markets are basically hoping for and largely positioned for a 50 basis point cut in July,” but a payroll gain around consensus means probably just a 25 basis point move.

- A sub-100,000 reading is needed for confidence in a half-point cut.

- Gain of 160,000 or more would send bond yields and the dollar up, while both would drop if it’s 100,000 or fewer.

- Equities could rise unless payrolls are quite weak, such as with a decline.

Chris Weston, head of research at Pepperstone Group in Melbourne:

- “Payrolls could cause a sell-off in bonds, but we’d need to see a huge number and far in excess of the consensus of 160,000.”

- “This is a world looking to buy any pull-backs in bonds, and funds have been pushed further out the curve in a bid for yield.”

Vishnu Varathan, head of economics & strategy at Mizuho Bank Ltd. in Singapore

- “If numbers fall short of rebounding back to 150,000-180,000,” then markets will be convinced of a July cut, he said.

- If payrolls are on the stronger side of the 100,000 to 200,000 range, “there could be some flattening of the two-year, 10-year yield curve, led by shorter-end yields edging up, he said.

Masanari Takada, cross-asset and quantitative strategist at Nomura Holdings Inc. in Tokyo:

- “Macro-oriented traders could turn bullish on stocks and thereby draw out even more buying by commodity trading advisors.”

- “On the other hand, CTAs might start dismantling their long positions if macro traders were to become even more guarded. We still have a bullish view on global stocks in July and think that the former of these two scenarios is the more likely one.”

Stephen Innes, a managing partner at Vanguard Markets Pte. in Singapore

- “Unless it comes in well beyond reach on both the headline and wages, it will not make one iota of difference to the Fed.”

- “They need to make a credible policy stance around trying to ignite inflation and should go 50 basis points in July.”

Binay Chandgothia, portfolio manager at Principal Global Investors in Hong Kong:

- “If, alongside decent growth in employment, wage growth also recovers, it will help push yields higher. It will be slightly positive for equities as well, though not as much as the impact on bond yields.”

- “A weak number will keep yields well bid and increase the probability of a 50 basis point rate cut later this month. Equities may correct a little but the prospects of a faster Fed response will prevent a larger draw-down.”

- “The only debate is whether the Fed can pivot to a 50 basis point rate cut and then stay on the sidelines to see the impact of such a cut for a few months.”

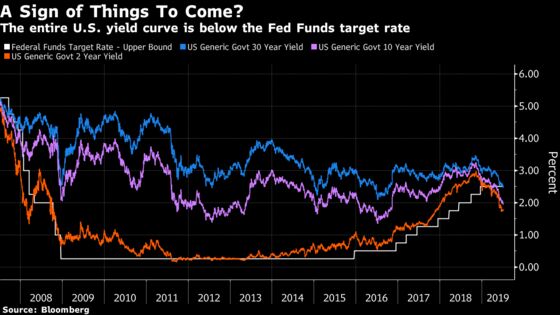

Shyam Devani, senior technical strategist at Citigroup Inc. in Singapore

- “The inverted curve in the U.S. is unavoidable, as it has been for a while now.”

- “U.S. 30-year yield is below the upper bound of the Fed Funds rate for the first time in more than 11 years. I don’t think this should, or can, be ignored.”

- “The NFP numbers today will either speed up the path to rate cuts or slow it down, but not derail the journey”

Dwyfor Evans, head of Asia-Pacific macro strategy at State Street Global Markets in Hong Kong

- “New highs in equities coupled with the inversion of the U.S. yield curve speaks of opposing forces in markets that should be ripe for an adjustment.”

- Dovish global central banks are “also opening up a large opportunity for EM, both in equities and particularly highly-rated sovereign bonds.”

--With assistance from Joanna Ossinger.

To contact the reporter on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Joanna Ossinger

©2019 Bloomberg L.P.