HelloFresh Proving Doubters Wrong After Slump, Analysts Say

HelloFresh Proving Doubters Wrong After Slump, Analysts Say

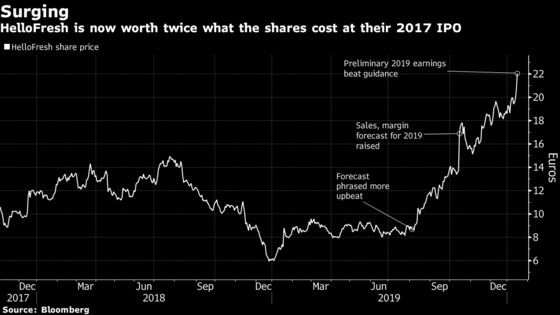

(Bloomberg) -- HelloFresh SE’s strong preliminary figures for 2019 help overcome the skepticism its business model has faced, yet the skyrocketing shares may have gone too far too fast, according to analysts.

There’s a good chance the company generated positive free cash flow last year, the “final proof of concept” for its meal-kit business, Bankhaus Lampe said. Even so, Morgan Stanley noted that much of the excitement is now priced in.

The German firm, which assembles ingredients into boxed meal kits that customers cook at home, jumped as much as 14% on Thursday, making an intraday record at 23.65 euros. A little more than a year ago, the stock had fallen below 6 euros.

While the current share price has overshot the target of even the most bullish of the eight analysts surveyed by Bloomberg, none of them recommend selling the stock, five rating it buy and three advising to hold. The company will publish its full annual report on March 3.

The stock has more than doubled since the initial public offering in 2017, making it one of Germany’s most successful listings above $50 million of the past five years.

| Company | offer-to-date performance | IPO date |

|---|---|---|

| Varta AG | 371% | Oct. 2017 |

| Hapag-Lloyd AG | 287% | Nov. 2015 |

| Siltronic AG | 194% | June 2015 |

| Delivery Hero SE | 173% | June 2017 |

| Scout24 AG | 106% | Oct. 2015 |

| HelloFresh AG | 102% | Nov. 2017 |

Here is what analyst said following the earnings release:

JPMorgan, Marcus Diebel

- “Against much skepticism, business model has proven robust” with market share gains, strong customer growth and new launches in several countries

- While unlikely to occur short term, the risk of rising competition from Amazon/Whole Foods, HomeChef/Kroger or U.S. peer Blue Apron remains

- After today’s share price performance, “much of the excitement is now priced-in.”

- Rating neutral, price target 20 euros

Bankhaus Lampe, Christoph Bast

- Good chance company generated positive free cash flow in 2019, the “final proof of concept” for its meal-kit business

- HelloFresh is now the leading meal-kit provider worldwide with market share of 50% in U.S. and as high as 90% internationally

- Management established strong track record and raised its revenue guidance four times in a row

- Rating buy, price target 20 euros

Barclays, Alvira Rao

- Revenue beat is “impressive”

- Momentum of U.S. segment stronger than expected

- Margins much better than expected, demonstrating the unit economics of the model can indeed work

- Rating overweight, price target 19 euros

Morgan Stanley, Miriam Adisa

- Expects “significant” Ebitda upgrades as HelloFresh’s operating profit beats the highest analyst estimate.

- Rating equal-weight, price target 17 euros

--With assistance from Nate Lanxon, Kit Rees and Lisa Pham.

To contact the reporter on this story: Richard Weiss in Frankfurt at rweiss5@bloomberg.net

To contact the editors responsible for this story: Daniel Schaefer at dschaefer36@bloomberg.net, Kasper Viita, Paul Jarvis

©2020 Bloomberg L.P.