Having the Biggest Corporate Jet Doesn't Always Help

Having the Biggest Corporate Jet Doesn't Always Help

(Bloomberg Opinion) -- By rights, wealthy finance types should adore Bombardier Inc. The Canadian aerospace and train manufacturer’s Global 7500 is the biggest business jet around and can fly non-stop from New York to Hong Kong reaching almost the speed of sound. It’s yours for a mere $73 million.

To describe the cabin as roomy is an understatement. There are four separate “living spaces” and a kitchen in which a Michelin-starred chef would feel at home. Sadly for Bombardier, investors are more interested in the company’s cash flow statement right now than in the wonders of its flying palace.

In theory, Bombardier has moved on from the balance sheet and liquidity crisis that almost sunk it in 2015. The company secured capital injections from Quebec, slashed thousands of jobs and offloaded assets, including a majority stake in the long-delayed C Series commercial aircraft to Airbus SE.

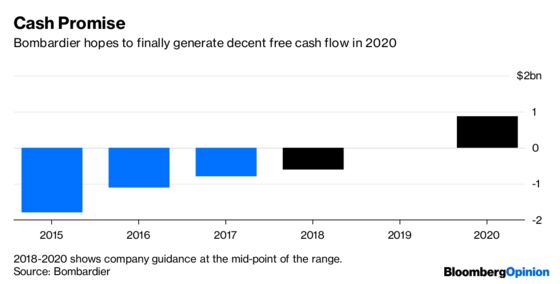

The Global 7500 is the chief reason for optimism about Bombardier’s fortunes. It expects group sales will grow by an average of 10 percent each year until 2020 as the jet enters service. Analysts surveyed by Bloomberg think the stock could double in the next 12 months. None has a sell recommendation. “Bombardier is a much stronger company in 2018,” chief executive Alain Bellemare assured them at a capital markets event in New York this week.

Yet the company’s shares and bonds paint a less cheerful picture. The stock has slumped 60 percent since a peak in July, to levels seen when Bellemare was still staving off the crisis in 2016. Bombardier’s 6 percent bonds due in 2022 trade well below par. That’s hardly reassuring when there’s $9.5 billion of debt and several big bond issues maturing in the next few years.

The problem is that Bombardier still doesn’t generate cash. Because of the amount of working capital tied up in large train projects – including London’s delayed Crossrail project – it will probably burn through several hundred million dollars this year (excluding divestment proceeds). Next year, it will be close to breaking even on a cash basis.

Bellemare insists this is all temporary. The working capital effects should reverse eventually, while capital expenditure is declining as major investment programs complete. Meanwhile, earnings should increase as Bombardier delivers its orders. Hence, it should generate at least $750 million of cash in 2020.

All of this is plausible. He’s already done a lot to lift profitability at various business units. There are fewer things that could go disastrously wrong. While it was a blow to Bombardier's pride, giving away most of the C Series was sensible given the drain on the company’s resources.

But the company still looks pretty desperate for money. It sold a big parcel of land in Toronto earlier this year and is now divesting its Q400 turboprop and flight training divisions. It also makes extensive use of factoring, where a business sells its invoices to a third party – at a discount – to get paid quickly. No wonder. The interest on its debt eats up about $650 million annually, although it should have $3 billion of cash on hand at the end of the year.

Unfortunately, it’s hard for investors to feel 100 percent confident about cash flow forecasts, which are inherently difficult in the capital-intensive train and aircraft industry. Suppliers, technical difficulties and regulators often cause unexpected hold-ups.

In other words, telling investors that Bombardier has a brighter future is one thing. A highly-leveraged business has to do more than that though. Bellemare needs to show shareholders the money too.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.