When the Going Gets Tough, Markets Cast Blame Everywhere

When the Going Gets Tough, Markets Cast Blame Everywhere

(Bloomberg Opinion) -- Last week showed you all you need to know about how traders and investors instinctively react when markets get choppy. They’re dazed, confused and quick to cast blame.

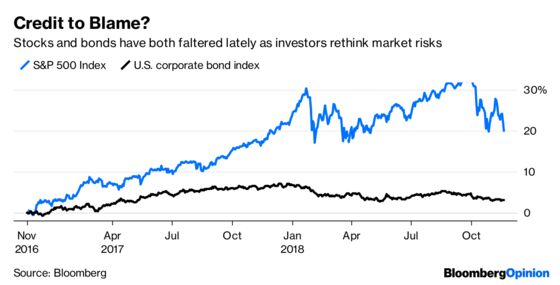

Consider Tuesday, when the S&P 500 Index capped a two-day decline of 3.5 percent to close near the lowest level since May. “The stock market has a debt problem,” a Bloomberg News article declared, highlighting that shares of companies with higher ratings have held up better than those with weaker credit profiles. Conceptually, that makes sense, given the handwringing over the fate of General Electric Co., viewed as the poster child of a flailing company with too much debt. It’s hanging on to ratings in the lowest investment-grade tier as its stock price hovers near the lowest since the financial crisis.

Less than 24 hours later, though, investors were trying to flip the narrative. “Credit is simply moving in sympathy with febrile sentiment in stocks,” another Bloomberg News article said. “I don’t care how smart it sounds to say ‘credit is leading the way,’” said Peter Tchir, head of macro strategy at Academy Securities. “It just isn’t correct.” It’s not? But I was just informed that it was.

Whiplash, finger-pointing and contradictions. Stepping back to see it for what it is might be the most instructive thing of all for investors looking to rise above the day-to-day noise. No, it’s not as simple as blaming “cracks” in credit for the recent losses in equities. And no, weakness in corporate bonds isn’t just a function of stock market volatility. As Neil Irwin put it in a recent New York Times headline, “Markets Are Revealing the Sum of All Risks.” What about U.S. Treasury yields that just won’t stay down? What about a Federal Reserve that may or may not pause, and the implications of either scenario? What about America’s persistent battle with China over trade?

What we are witnessing, it seems, is a fundamental shift in the investing landscape. Since the recession ended in June 2009, few strategies would have outperformed the simple mantra of “When in doubt, buy stocks.” For bond traders, the move has likewise been “When in doubt, reach for yield.” There’s reason to believe that sort of thinking isn’t going to work so well anymore. Bridgewater Associates’s Ray Dalio said last week that “We’ve pushed assets up to levels where it is difficult to see where you can squeeze that,” meaning overall returns may be lower for a long time.

Unsurprisingly, markets aren’t taking kindly to this outlook. Younger traders have never even seen a long-lasting downturn in risk assets. The current whipsawing of stocks has persisted for seven weeks, and unlike the burst of volatility that began in February, it seems harder to write off this time as an isolated episode. Not to mention that the Fed has raised interest rates three times since then and seems ready to go in December, even as the market’s inflation expectations crumble and stocks look for the magical “Powell put” that will stem losses.

I won’t pretend to know how this will all shake out. I just know that casting specific blame in the heat of the moment— whether it’s stock valuations, interest rates and the Fed, the price of oil or corporate leverage — is a fool’s errand. The one thing everyone can agree on is that markets are interconnected. It was easy to remember that when most assets were rising in tandem. But it’s even more vital to keep in mind when many are on the decline.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.