Subprime Lender's Deal May Herald More Bonds With 100%-APR Loans

Have a 100%-APR Consumer Loan? This Lender May Securitize It

(Bloomberg) -- Online subprime lender Enova International Inc. bundled consumer loans with eye-popping interest rates -- some topping 99 percent annually -- into bonds last year. And there may be more such debt deals to come.

The deal reflects online lenders’ growing focus on non-prime borrowers -- what Enova calls a "large, expanding market segment" in a November public investor presentation on its website. The company estimates there are at least $69 billion of untapped non-prime lending opportunities for unsecured consumer loans in the U.S. alone.

The subprime consumer-loan industry may now get a boost under a proposed rule issued Feb. 6 by CFPB Director Kathleen Kraninger that would remove the requirement for payday lenders, auto title lenders and certain installment lenders such as Enova to determine a borrower’s ability to repay the high-interest rate, short-term loans. Fair-lending advocates warn that the proposed change will erode consumer protections.

It turns out some of these high-cost loans have gone into bond deals. Enova’s $125.4 million unrated bond issue securitized so-called installment loans from its "near-prime" consumer product line. Investors were rewarded for the elevated risk with yields as high as 7.4 percent for an unrated, 2.2-year slice of the transaction, according to data compiled by Bloomberg News. And thanks to structural protections and enhancements built into the transaction, it is arguable that the bond is relatively safe.

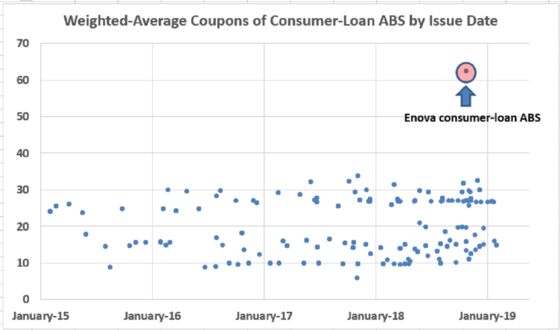

However, the deal’s batch of bundled underlying loans had an overall weighted-average coupon of 62.86 percent, compared to an average of only about 20 percent for other consumer-loan-backed bonds from issuers such as OneMain Financial Inc., Social Finance Inc., and Oportun Financial Corp., the Bloomberg data show.

This is largely explained by the fact that Enova specializes in non-prime borrowers, whereas many other online lenders do not. Even so, the Enova rates may be on the high side. Personal-loan annual percentage rates (APRs), even for people with weak credit scores (300 to 639 FICOs), typically max out at 32 percent, according to consumer-spending data website ValuePenguin. An investor relations representative from Enova declined comment because the bond was a privately issued transaction.

Enova offers "near-prime" borrowers loan APRs ranging from 34 to 155 percent, loan sizes from one to ten thousand dollars and maturities from six to 60 months. A separate subprime product offered by the company, called CashNetUSA, offers smaller-size loans with APRs reaching as high as 450 percent, according to its website.

Enova, one of the largest U.S. online subprime consumer lenders, has diversified away from so-called payday or single-pay loan products in recent years and pivoted toward installment loans, which are paid back over time rather than in a single payment. Its competitors, such as Curo Group Holdings Corp. and Elevate Credit, Inc., have made a similar move, especially as payday lenders, who charge wildly high APRs for short-term loans, have been widely criticized for potentially creating "debt traps" for vulnerable borrowers.

While many installment loans also have ultra-high interest rates, their structure, size, and maturities often mitigate the risks, though some fair-lending advocates still warn borrowers to be wary of the product. But Enova’s expansion into installment loans and lines of credit has paid off so far: the company exceeded its revenue targets, according to its fourth-quarter earnings call last Thursday, with its U.S. business increasing revenue 31 percent year-over-year.

"The ongoing diversification of our receivables portfolio continues to generate faster receivables growth in our line-of-credit and installment-loan products," CFO Steven Cunningham said on the call. Domestic near-prime installment loans grew 27 percent year-over-year and comprised 45 percent of total receivables at the end of the quarter, he added.

And those high-interest-rate loans may continue to end up in securitization transactions. The consumer-loan sector has become a more frequent user of the asset-backed securities bond market, which offers issuers a lower cost of capital and an expanded investor base. Bonds backed by unsecured consumer loans reached $30 billion outstanding at year-end 2018, or roughly double the amount of bonds backed by retail credit card payments, analysts at Wells Fargo & Co. wrote in a research note yesterday. Last year saw $12.3 billion of new U.S. consumer-loan asset-backed bonds, up from about $9 billion in 2016, according to data compiled by Bloomberg News.

"As the sector has grown, rating agencies and investors alike have grappled with the short lending histories of the companies, loan performance and the pricing of risks," Wells Fargo analysts John McElravey and Ryan Brinkoetter wrote in their report.

--With assistance from Kristina D'Alessio, Kyle Ashworth and Charles Williams.

To contact the reporters on this story: Adam Tempkin in New York at atempkin2@bloomberg.net;Christopher Maloney in New York at cmaloney16@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Allan Lopez, Dan Wilchins

©2019 Bloomberg L.P.