GrubHub Plunges as Analysts See No Silver Linings in Results

GrubHub Plunges as Analysts See No Silver Linings in Results

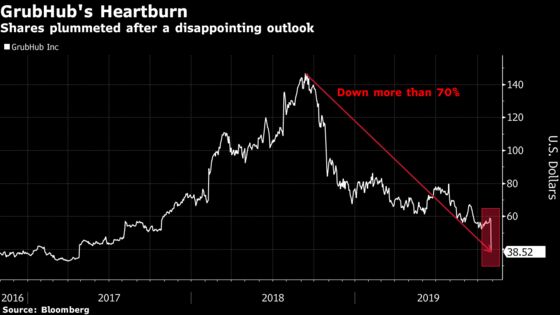

(Bloomberg) -- GrubHub Inc. shares plummeted to their lowest level in more than two years on Tuesday, after the food-delivery company gave a fourth-quarter outlook that was well below expectations, as intensifying competition and “promiscuous” customers weighed on growth trends.

“Newer diners are increasingly coming to us already having ordered on a competing online platform, and our existing diners are increasingly ordering from multiple platforms,” Chief Executive Officer Matt Maloney and Chief Financial Officer Adam DeWitt wrote in a letter to shareholders. The company nodded to newer entrants like DoorDash and Uber Eats and wrote that competition “had a 300+ [basis point] impact on our growth rate for the third quarter.”

In the company’s conference call, GrubHub’s management subsequently said that “growth had deviated noticeably from where we thought it was going to be” in the quarter.

Analysts were extremely bearish on the results, with at least three firms lowering their ratings and others slashing their price targets. The average target currently stands at about $76, according to date compiled by Bloomberg, down from $87 over the weekend.

While investors had been bracing for a weak outlook, Wedbush wrote, “it certainly was not at this order of magnitude.” BTIG added, “we struggle to find any silver lining in these developments.”

There was also caution around GrubHub’s plan to invest aggressively in order to protect its market share. While there is a business case to be made for this, Stephens wrote, it “significantly pushes out the earnings story and again sets up GRUB as a ‘show me’ stock for 2020.”

Shares plunged 42% in their biggest one-day drop ever, with the stock trading at its lowest since April 2017. With the decline, the stock has dropped more than 70% from a peak in September 2018.

Here’s what analysts are saying about the results:

Oppenheimer, Jason Helfstein

GrubHub usage is “eroding,” and this trend is “expected to worsen” in the fourth quarter.

In order to compete, GrubHub “will now focus on lower margin features.” There is “limited investor demand with slowing growth and declining Ebitda.”

Downgrades to underperform from outperform; price target cut to $34 from $91.

BofA, Nat Schindler

Downgrades by two notches, to underperform from buy. Price target slashed to a Street-low view of $30 from $98.

“The food delivery market is increasingly irrational as competitors flood the market,” making customers less loyal to any particular company. The company’s “answer to this irrationality, however, seems confusing: its management letter seems to suggest that it will double down on its competitors’ poor economic decisions,” including free delivery for quick service restaurants.

These strategies “should attract customers with lower order frequency and less lifetime value, reducing [long-term] profitability while providing little real growth.”

Craig-Hallum Capital Group, Alex Fuhrman

The outlook “creates a bleaker picture in the short-term.”

Decelerating revenue growth, along with Ebitda pressures, “creates a challenged environment for the stock, with investors now likely needing to see a stabilization in revenue growth coupled with improved profitability.”

Downgrades to hold from buy, price target cut to $40 from $100.

Jefferies, Brent Thill

The weaker-than-expected third-quarter results are “the least of the issues,” given the “drastically reduced” outlook and the “aggressive spending” to reinvigorate growth. The spending plan “makes sense given the circumstance,” but “there is no guarantee that it will change the overall narrative.”

The company “has turned into a revenue deceleration story with compressing margins all in the face of increased competition, not a great recipe for success.” Expects increased consolidation in the food-delivery sector, but this is “a challenging industry to truly differentiate (especially against two deep-pocketed competitors).”

Hold rating, price target cut to $45 from $78.

Stephens, Will Slabaugh

There is a business case to be made for increasing investments in order to protect market share, but “this significantly pushes out the earnings story and again sets up GRUB as a ‘show me’ stock for 2020.”

Currently has an overweight rating and $110 price target, but the view is under review.

Cowen, Thomas Champion

“The growth and profitability picture looks much worse than we previously thought,” with “multiple headwinds” cited as cause for concern.

Management’s commentary “suggests tempered expectations make sense, with future growth coming from areas like take-out and driving lower diner-facing fees.”

Outperform, $86 price target.

BTIG, Peter Saleh

“We struggle to find any silver lining in these developments,” and the slowdown “has caught us by surprise.”

“We are unclear as to the path forward from here,” although industry consolidation is likely.

Affirms buy rating, and $95 price target, but adds that estimates are under review until the conference call.

Wedbush, Ygal Arounian

The outlook represents “a full-on kitchen sink moment as GrubHub finally gives in to competitive dynamics.”

While investors had been bracing for a weak outlook, “it certainly was not at this order of magnitude.” This is “clearly a full reset of expectations,” and GrubHub management “will face a steep climb in an effort to regain Street credibility.”

Despite the “decidedly negative” report, affirms outperform rating and $90 price target pending the conference call.

What Bloomberg Intelligence Says:

The quarter “validates our premise that the company is facing intense competitive pressure.”

“The company’s smaller scale remains a disadvantage against larger peers such as Uber Eats and DoorDash.”

- Analyst Mandeep Singh

- Click here for the research

To contact the reporter on this story: Ryan Vlastelica in New York at rvlastelica1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Brad Olesen

©2019 Bloomberg L.P.