Amazon Threat Squelches Industrial Good Vibes

Amazon Threat Squelches Industrial Good Vibes

(Bloomberg Opinion) -- Grainger is weathering competition from Amazon.com Inc. better than some expected it would, but it’s still feeling the pinch.

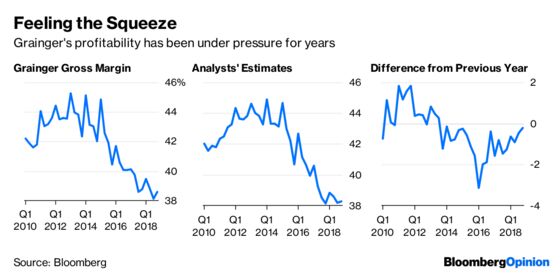

Amazon’s push into the distribution of factory-floor basics and office supplies has forced incumbents like W.W. Grainger Inc. to cut prices and revamp their online strategy to keep up. The result has been shrinking gross margins and a sales boost that looks temporary, evidence of which was present on Thursday when Grainger reported fourth-quarter results and gave its 2019 outlook. To give the company credit, its gross margin in the fourth quarter of 38.6 percent was better than analysts expected and surpassed management’s own guidance. But this was still the 21st straight quarterly decline in that profit gauge – and there’s the potential for more slippage in 2019.

Grainger estimated it will retain between $38.10 and $38.70 in gross profit from each dollar of sales in 2019, with the middle of that range implying a drop from a year earlier and falling short of analysts’ estimates. The company had previously vowed to hold its gross margin stable, so this would appear to be a lowering of that target (I will acknowledge, though, that maintaining the goal would have been more challenging, given Grainger’s better-than-expected performance on this metric).

Grainger did reiterate its target of reaching an operating margin of 12.2 percent to 13 percent in 2019, a goal that watchers of the company including myself had bashed as unrealistic. Grainger notched an adjusted operating margin of 12 percent in 2018, a performance that would appear to make the 2019 target less of a stretch. I will note, however, that the adjustments include $47 million of restructuring expenses and a $139 million non-cash impairment charge related to Grainger’s U.K. Cromwell business. You can debate whether restructuring charges are truly one-time for a company like Grainger that’s facing a structural reset. And the Cromwell business likely faced pressure from Amazon, which introduced its business-to-business offering in the U.K. in 2017. The company’s unadjusted operating margin in 2018 was 10.3 percent.

Beyond the Amazon threat, the reason these metrics matter so much is that Grainger’s plan for rebuilding its profitability depends on continued growth in sales volume. If it can’t deliver when sales are strong, how is it going to fare when the momentum starts to wane? That already appears to be happening. The company’s fourth-quarter revenue was lower than expected and volume growth of 4 percent made the period the weakest of the year. Grainger expects to deliver 4 percent to 8.5 percent sales growth in 2019. It didn’t specify the volume gains baked into that forecast, and it’s notable that Grainger’s previous call for volume growth of 6 percent to 8 percent in 2019 doesn’t appear in the earnings materials. Recall that Grainger had already attempted to water down that target by rebranding it as a collective goal for 2018 and 2019. CEO DG Macpherson on Thursday said only that he remains confident in Grainger’s ability to deliver above-market volume growth.

Wednesday’s batch of industrial earnings provided needed relief for battered investors. United Technologies Corp. soared the most since 2009 after reporting its strongest organic sales growth since before the financial crisis, and as it gave more details around its planned breakup. United Rentals Inc., which reported after the close on Wednesday, also surged after posting a 20 percent pop in fourth quarter-sales and reiterating the rosy 2019 outlook it gave in December. It’s proof that there are pockets of continued strength in the industrial sector that counter the slowdown narrative. Grainger just isn’t one of them.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.