Goldman Sachs Sees ‘New Conundrum’ Capping Treasury Yields Surge

Goldman Sachs Sees ‘New Conundrum’ Capping Treasury Yields Surge

(Bloomberg) -- Bond buyers face a “new conundrum” where Treasury yields will stay low even as the Federal Reserve hikes rates, despite the surge in the first week of the year, according to Goldman Sachs.

The investment bank expects the bond market to be reluctant to lift the terminal rate during the coming tightening cycle. So while raising its year-end forecast for the two-year yield, its calls for longer-dated yields stand. Goldman projects the five-year note to end 2022 at 1.8%, the 10-year to climb to 2% and the 30-year to reach 2.25%. A Bloomberg survey of 2022 predictions for these Treasury benchmarks shows median yields of 1.63%, 2.01% and 2.40%, respectively.

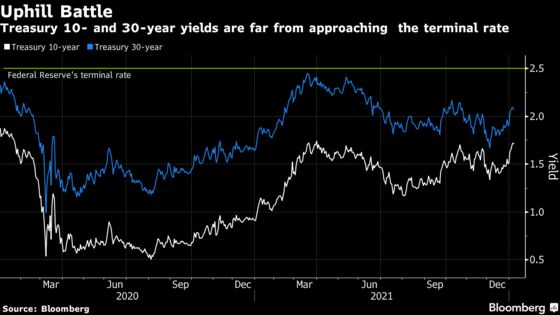

The Fed’s long-term estimate for its overnight borrowing rate is 2.5% during the current economic cycle. But the bond market has consistently lagged that view based on its prevailing low yields on long-dated Treasuries. Inflation expectations and long-dated nominal yields have remained relatively contained while the Fed has expressed concerns about rising prices, is tapering bond purchases and expects to implement three quarter-point rate hikes this year.

This backdrop suggests the Fed is setting itself up for a reprise of the tightening cycle in the early 2000s when long-dated Treasury yields remained low even as the central bank hiked, a pattern that then Fed chair Alan Greenspan described as a “conundrum” in early 2005.

Strong Demand

“There are two possible explanations” for the new bond market conundrum, according to Goldman, “a widely prevalent low terminal rate view, or that the price signal is distorted by supply/demand imbalance.” The Wall Street giant said the imbalance between supply and demand is “a more compelling” explanation, adding that it’s “one that will take time, and some rate hikes to resolve, leaving the long end relatively sticky over the course of the year even as front end yields reprice materially higher.”

Foreign demand for U.S. Treasuries remains high as other sovereign yields are negative or near zero, a point raised by Fed chair Jerome Powell after last month’s central bank meeting. In recent years, large institutional investors including pension funds and insurers have also been buyers of 30-year Treasuries when yields have risen above 2%, which is seen as reflecting expectations for a low terminal funds rate.

This week’s Treasuries selloff has been more focused on the front end as the market has boosted the odds of the first rate hike arriving in March, rather than May. As a result, the yield curve has flattened, with 10- and 30-year yields lagging the rise in two- and five-year notes.

Goldman has increased its year-end estimate for the policy sensitive two-year note yield to 1.35%, from 1.15%, as its economists now project “three hikes by the end of 2022, and a steady three hikes per year pace thereafter.”

©2022 Bloomberg L.P.