Gilead Risks Regrets on Pricey Galapagos Partnership

Gilead Risks Regrets on Pricey Galapagos Partnership

(Bloomberg Opinion) -- Gilead Sciences Inc.’s new CEO Daniel O'Day is trying to replicate the successful playbook of his former employer Roche Holding AG, the Swiss pharma giant he worked at for more than 30 years.

On Sunday, Gilead announced that it would invest $5.1 billion to deepen an existing relationship with Belgian biotechnology firm Galapagos NV. O'Day isn't just committing to Galapagos – he’s committing to the idea of research partnerships that stop short of outright M&A. The deal includes a 10-year standstill agreement that restricts Gilead's ability to acquire the company.

O'Day thinks that leaving Galapagos independent will keep it innovative, a bet that paid off for Roche and its productive long-term partnerships with Genentech and Chugai Pharmaceutical Co. That nebulous benefit will have to come through in a big way to justify the price and structure of this deal.

Gilead is paying $3.4 billion upfront to gain rights to six drugs in clinical trials and access to a suite of earlier-stage programs. It is also making a $1.1 billion equity investment in Galapagos.

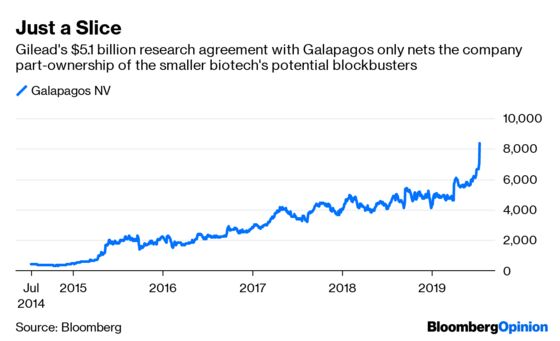

The total outlay is a scant $2 billion less than the market cap of Galapagos before the deal was announced, and is above what the company was worth as recently as March. On top of that, Gilead already owned 12 percent of Galapagos and rights to potential blockbuster arthritis drug filgotinib from a $725 million deal completed in 2015. O'Day also isn't done paying up. He will have to shell out more cash to opt in to future programs and for development costs. Gilead will also pay a significant sales royalty if any drugs are approved. And Galapagos will retain European rights for most of its medicines.

The potential return of this deal is lower than an outright acquisition, and Gilead didn't seem to get much of a discount. It’s giving up a lot to limit its risk and test the abstract notion that partnerships are superior. The company's late-stage pipeline is sparse, and it is too reliant on its HIV franchise. It’s not in a position to leave upside on the table.

There’s a chance that the deal could work out. Gilead’s only has to pay $150 million to gain exposure to programs that are currently in early stages; that could wind up being a relative steal at some point in the next decade. Investors may feel a twinge with every opt-in and royalty check, however.

Gilead had chances during the past few years to acquire Galapagos at a lower price than what it’s paying for the partnership now. That feels like a missed opportunity, and may seem even more so if its pipeline and R&D platform turn out to be as strong as O’Day seems to think they are.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.