Germany’s Economy Will Be Europe’s Problem

Germany’s Economy Will Be Europe’s Problem

(Bloomberg Opinion) -- The imminent end of German Chancellor Angela Merkel’s final term presents a great challenge for both her country and the entire European project. If her successor can’t pull the German economy out of its slide toward second-tier status, the union could lose its most important financial supporter.

Since Merkel’s announcement that she will not seek another term in 2021, the focus has been on whether her successor will be more willing to engage in the kind of risk-sharing needed to make the euro a viable currency — meaning a more complete banking union and more fiscal support for struggling member countries. Friedrich Merz, a leading contender to replace Merkel, has implied he might try, though he remains skeptical of “old French ideas” for financing deeper integration.

Yet even if Germany’s next leader can summon the political will, there’s another obstacle: a diminishing economy, which threatens to undermine the confidence Germans need to play a more proactive role. Besieged on multiple fronts, the country is struggling to deliver higher standards of living. For nearly half the population, incomes haven’t risen in a generation.

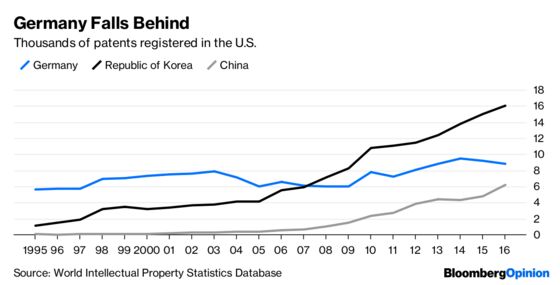

The warning signs flashed in Merkel’s first term. German companies, for example, had long excelled in innovation, as measured by the number of patents registered in the U.S. But by 2007, Korean companies had caught up. They now register nearly double the number that their German counterparts do, thanks to huge investments in education and research. China, too, has been gaining ground, joining Korea in staking a claim to global technological leadership.

Merkel understood the challenge. In 2010, she promised a big push on investment in education and research. She invoked Europe’s Age of Enlightenment in the 17th century, when dazzling intellectual progress placed Europeans at the frontier of human knowledge. She recognized that Chinese leaders were making a concerted bid to return to the heyday that Chinese science enjoyed in the 10th century.

But Germany fell short. As of 2015, Korean and Chinese high-school students were outperforming their German counterparts in science and, especially, in mathematics. While Korean universities have not securely established themselves in the top echelons, the two best Chinese universities rank higher than the best German universities. Indeed, measured by how often their science and technology research is cited, Chinese universities occupy the top two spots globally and four more of the top 15. No European institution is even on that elite list.

The automotive industry exemplifies how Germany is losing its edge. The country has long enjoyed a formidable reputation for quality, performance and style. But that might be changing. In an ever-enlarging scandal, American and European regulators have caught German companies cheating on emission standards in their diesel cars. As they scramble to meet the standards, the country’s automakers are facing a broader regulatory transformation, with municipal authorities banning cars in city centers.

Meanwhile, as electric replaces internal combustion, German manufacturers remain deeply rooted in the old diesel technology. Merkel and her government have sought to ease their pain by delaying tougher emission standards and deferring bans on car use, but this is a losing battle. Germans place a premium on cleaner air. The transition to electric cars will render the technologies used by automakers and their suppliers largely obsolete, causing wide-ranging disruption.

There’s more. Germany’s fabled banks have served the country’s small and medium-size firms well. But the banks suffer from chronically low profitability — particularly in the network of quasi-public institutions, the Sparkassen and Landesbanken, typically owned or controlled by municipalities and state governments. In 2001, the European Commission pronounced that the Landesbanken were receiving unfair subsidies. As they lost access to the subsidies, the Landesbanken gambled for redemption in the U.S. subprime market and other risky ventures. Predictably, they bled profusely.

Perhaps Germany’s greatest weakness is Deutsche Bank, whose stock price is still less than a tenth of where in stood in May 2007, ahead of the subprime crisis. In recent years, U.S. and British regulators have fined the bank hundreds of millions of dollars for improper representations and possible money laundering. It’s currently under separate investigations for assisting criminals and Denmark’s Danske Bank in laundering large sums of money. Its business model is evidently not working. If it falters, its size and global systemic connections could place a substantial burden on the government.

Ideas propel a modern economy. Yet Germany’s farthest-reaching economic policy of the past generation, the labor reforms of Gerhard Schröder, reduced incentives to invest in human capital by making it easier to fire employees. Workers became expendable, inequality increased and the sense of insecurity spread. Climbing the economic ladder became harder. Many discouraged Germans turned to the euroskeptic, anti-immigration Alternative für Deutschland party. A growing rebellion within Merkel’s Christian Democrats eroded her authority. These deepening political fault lines delivered a fragmented German Bundestag in the 2017 federal elections, placing Germany’s vaunted political stability at risk.

Germany must shed its narrow reliance on engineering excellence and bank funding, and move toward a more flexible structure where emergent technologies can flourish. This primarily requires the scale of investment in education and curriculum modernization that Merkel hinted at but did not deliver. Education is twice blessed: It fosters growth and gives hope to those left behind. The government must also consolidate the Sparkassen and Landesbanken into two or three banks, while severing their subsidies. And if Deutsche Bank is not cleaned up and downsized, it will surely become a public liability.

Economic historian Charles Kindleberger described a hegemonic power as one that makes short-term financial sacrifices to aid other countries, believing that prosperity elsewhere comes around to benefit it. Germany is in the last phase of its global prominence, a nation unwittingly sliding into the ranks of also-rans. The question is whether it’s too set in its ways, with too many vested interests, to change course.

The task for the next chancellor is clear: Reinvigorate the economy. Only then will Germans show a willingness to do more for Europe.

To contact the editor responsible for this story: Mark Whitehouse at mwhitehouse1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ashoka Mody is a visiting professor in international economic policy at Princeton University. Previously, he was a deputy director at the International Monetary Fund's research and European departments. He is the author of "EuroTragedy: A Drama in Nine Acts."

©2018 Bloomberg L.P.