GE Slashed Its Dividend. Not Us, Says Emerson.

GE Slashed Its Dividend. Not Us, Says Emerson.

(Bloomberg Opinion) -- What's an earnings report without a little shade-throwing?

Emerson Electric Co., the $44 billion maker of industrial automation equipment and InSinkErator food disposals, reported earnings on Tuesday, and a line from its statement caught my eye. CEO Dave Farr dedicated a whole paragraph of his commentary section to Emerson's shareholder payouts. The company spent $2.2 billion on buybacks and dividends in fiscal 2018, or 77 percent of its operating cash flow. Here’s what Farr had to say about it:

"[It’s] an important indicator of our financial strength and ability to continue increasing our annual dividend, as we have done every year since 1956. This unblemished 62-year track record is a testament to the extraordinary commitment of our employees, of our global management teams and of our board to deliver value to our shareholders.”

The dividend has always been a priority for Farr, of course. But at the same time, it's hard not to read those lines as a shot at General Electric Co. and its less pristine track record. Former CEO Jeff Immelt was forced to cut GE's payout during the financial crisis, an event he characterized as the worst day of his tenure. His successor John Flannery was forced to cut the dividend last year amid GE’s recent painful and unrelenting decline, admitting the company hadn't been generating enough cash flow from its industrial businesses to support the payout for years. Flannery lasted only 14 months in the job and his successor, Larry Culp, cut GE's quarterly dividend again last month to a token penny a share.

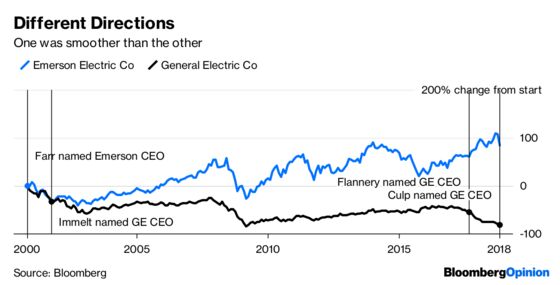

It's helpful context to remember that Dave Farr became Emerson's CEO in October 2000, about a year before Immelt ascended to the top post at GE. Here's a look at the two companies' stock prices over their tenures:

Farr perhaps shouldn't be throwing too many stones, if that’s what he was intending. Yes, he's never had to cut the dividend, but he's not perfect, especially when it comes to capital allocation, a sore spot for Immelt as well. Farr acquired backup power-equipment maker Chloride Group Plc for $1.5 billion in 2010, but had to take a $508 million charge on the deal a few years later, got his bonus docked and eventually sold the network-power unit that housed the Chloride operations. Several shareholders have told me they lost faith in Farr after his ill-advised, expensive pursuit of Rockwell Automation Inc. last year, which failed after the company rebuffed his offers.

His last few deals have been smaller and smarter, though, including the 527 million-euro ($622 million) acquisition of Rockwell mini-me Aventics in July and the recently announced takeover of GE's intelligent platforms automation business. And Emerson's business is performing well right now, as the company's strong fourth-quarter results show. Investors seemed spooked by weaker-than-expected guidance for fiscal 2019 and its forecast for a slowdown in organic sales growth from the blistering 8 percent pace Emerson posted for fiscal 2018. That adds to fears about peak earnings, as industrial companies combat rising raw material and freight costs as well as currency swings. But all the same, Farr looks set to retire from Emerson on a high note. At the very least, he can justifiably say his company is no GE. It's all relative, after all.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.