GE’s Health-Care Split Should Put Creditors First

GE’s Health-Care Split Should Put Creditors First

(Bloomberg Opinion) -- General Electric Co. CEO Larry Culp is honoring his promise to urgently address the company’s massive debt load. The best options to do so may be the ones that also give him the most flexibility.

The industrial conglomerate has reportedly filed confidentially for an initial public offering of its health-care unit, which sells MRI machines as well as cell-therapy technologies. This isn’t too surprising: Culp said in October that he agreed with the general thrust of former CEO John Flannery’s plan to make the health-care business an independent entity. But there was always the possibility he might change his mind, much like he did on the prospect of an equity raise, having first ruled it out before later indicating he might consider selling shares “as conditions change in the future.”

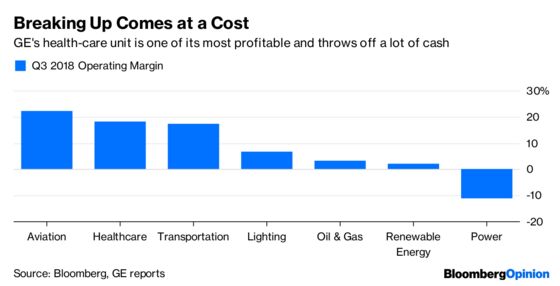

Some investors had hoped health care would stay in the fold. An IPO of the unit is essentially an equity raise by another name, but in that case, GE would be divesting its best cash-generating unit. The capital-intensive aerospace, power and renewables combination that will remain looks even more risky as recession signals flash yellow. Late Tuesday, FedEx Corp. cut its fiscal 2019 earnings guidance just three months after raising it in one of the strongest signs yet that global growth — and the profit gains that go with it — may have peaked. Industrial CEOs generally sounded optimistic on third-quarter earnings calls, but the rapid deterioration of FedEx’s economic outlook is a reminder of how quickly the tide can turn.

The alternative to divesting the health-care business is a more traditional stock sale, whereby GE would essentially be offering shares in the downtrodden power business and liability-ridden financial arm that have dictated its valuation of late. While Culp is now seemingly not not going to consider an equity raise, he still appears reluctant to do so, for some reason. His re-opening of the door to an equity sale struck me as more about realizing he never should have taken it off the table in the first place, as opposed to a sudden warming to the idea.

This is puzzling to me because an equity raise would seem to be a valuable arrow in Culp’s quiver. Yes, he would inevitably have to sell shares at a discount to a stock price that’s already bumping up against financial-crisis lows. But doing so would give GE resources to offset the many elastic liabilities at GE Capital, while easing the leverage concerns that are largely responsible for driving that share price so low in the first place. If Culp can mitigate GE’s debt problem, plenty of investors would be excited for the opportunity to bet on a comeback. The over-enthusiastic pops in GE shares after even the slightest inklings of good news is a testament to that.

But if he’s not willing to go down that path, Culp likely will need to modify Flannery’s plan to sell a 20 percent stake in the health-care business and spin off the rest to shareholders. Most of the leverage reduction from that proposal comes via offloading about $18 billion in debt and pension liabilities onto the new entity. What GE really needs, though, is cash. Culp has already alluded to the possibility of selling as much as a 49.9 percent stake in GE Healthcare, which would buy him significantly more breathing room. But the other question to think about is why GE needs to spin any piece of the health-care business off to shareholders at all.

Flannery was very concerned about balancing the interests of bondholders with those of GE’s aggrieved shareholders; the idea behind the spinoff was to echo the company’s merger of its transportation unit with Wabtec Corp. and give investors the ability to participate in the future growth of the health-care business. But the upside potential for GE’s core shares is likely range-bound until the company can get a handle on its liabilities, and there may be a better way to leverage health care to do that. The most obvious comparison is Siemens AG’s separation of its Healthineers arm, which competes with GE in medical imaging. Siemens IPO’d a piece of that business, but it retains an 85 percent stake, which it could conceivably sell over time to raise cash — and likely at a premium to the IPO price, given Healthineers' stock-price appreciation. GE is already treating the health-care unit like a piggy bank; why not consider a similar structure that would give it additional resources should the need arise?

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.