GE Downgrade Hits Company in a Debt Market It Once Ruled

GE Downgrade Will Lift Its Costs in a Debt Market It Once Ruled

(Bloomberg) -- A ratings downgrade this week may hit General Electric Co. in one particular bond market: short-term debt.

That’s where the manufacturing giant lost its near-top credit ratings on Tuesday. Without those ratings, at least some investors in IOU’s known as commercial paper won’t be willing to invest in GE’s debt anymore.

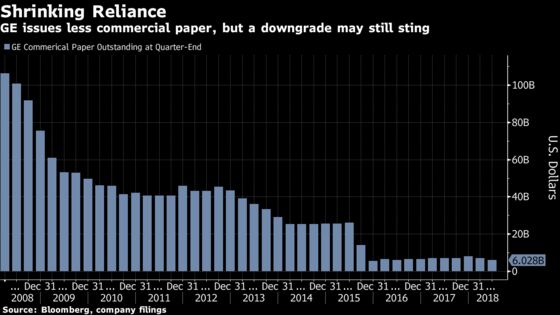

GE relies on commercial paper to help fund its daily operations, and it used to be one of the biggest issuers of the debt. The manufacturer had on average around $16.6 billion of the debt outstanding during the second quarter. At the end of June, it had about $115.6 billion of total debt, of which about $6 billion was commercial paper, according to company filings.

With fewer funds interested in buying at current ratings, GE will probably have to pay higher rates to sell its commercial paper, said Peter Crane, president of Crane Data, which tracks money market funds.

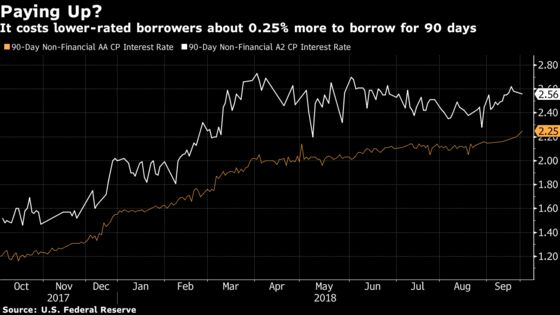

“They’ll still be able to find buyers, but at a cost of course," Crane said. On Monday, it cost 2.25 percent for a top-tier corporation to borrow for 90 days, according to U.S. Federal Reserve data. Companies the next tier down, where one ratings firm has GE, paid 2.56 percent.

Any increase in GE’s borrowing costs adds more pressure to a company that is already suffering. It’s facing sluggish demand for its gas turbines, flagging cash flow, and probes from the U.S. Securities and Exchange Commission. This week it replaced its chief executive officer with Larry Culp, the first ever outsider to head the company.

“GE has a sound liquidity position, including cash and operating credit lines,” said a GE spokeswoman. The company remains committed to strengthening its balance sheet, including reducing debt levels, she added.

S&P Global Ratings on Tuesday cut GE’s short-term grade to A-2, a level below the top tier. That’s a rating of commercial paper that some classic prime money market funds are reluctant to buy. Moody’s Investors Service has GE at P-1, or equivalent to one step higher than S&P, and said on Tuesday it may also cut the company’s short-term ratings.

Prime money market funds historically had to have at least 97 percent of their securities rated at least A-1 from S&P and P-1 from Moody’s, but those rules were loosened amid this decade’s money market reform. Even so, many of the funds are less willing to buy securities with at least one rating below A-1 or P-1, Crane said.

Less Reliant

S&P cut GE’s longer-term debt ratings as well, to BBB+ from A2, a two-notch downgrade that leaves the industrial giant at three steps above junk. That move is likely to have less impact on GE because the company’s longer-term bonds already trade like they’re rated in the BBB tier, and generally funds that can buy notes in the A range can also buy securities at GE’s current level.

One bright spot for GE’s commercial paper borrowing: it’s spent the last decade cutting its reliance on that market. In 2008, the company had more than $100 billion of the debt outstanding, making it one of the biggest issuers. But during the financial crisis, GE found its access to that market severely constrained, and vowed to change its liabilities. It turned to alternatives including longer-term corporate bonds and bank borrowing.

As GE has cut its reliance on commercial paper, the market has more broadly shrunk. In 2016, regulatory changes forced some prime money market funds to pass losses onto investors when short-term company debt lost value. That made funds that invest in only government securities more popular among some investors, sending assets in prime funds plunging.

“Money fund managers have primarily focused on bank commercial paper and only the highest, highest quality corporate paper," said Tony Carfang, a Chicago-based managing director at Treasury Strategies, a division of Novantas. “GE has been squeezed out."

--With assistance from Jason Feinstein, Misyrlena Egkolfopoulou and Richard Clough.

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2018 Bloomberg L.P.