Gannett Board Fight Does More Harm Than Good

Gannett Board Fight Does More Harm Than Good

(Bloomberg Opinion) -- The more MNG Enterprises Inc. tries to prove it’s serious about buying Gannett Co., the less credible it looks.

Gannett, the publisher of USA Today, earlier this week rejected the local newspaper owner’s $12-per-share takeover bid, saying it was too low and lacked key commitments on financing and antitrust. In response to that rebuff, MNG – which is controlled by hedge fund Alden Global Capital and better known as Digital First Media – announced late Thursday that it would nominate six directors to the Gannett board.

It’s highly unusual and needlessly aggressive to escalate an unsolicited takeover offer to a proxy fight after only one public bid. It feels like a distraction, considering MNG still hasn’t publicly addressed Gannett’s concerns about financing or regulatory hurdles with any degree of specificity. The two sides met on Feb. 7, and MNG said it addressed all of Gannett’s questions by reviewing a “path” to financing and “analysis” on antitrust matters. Those are nice words, but they don’t mean much in the absence of bank commitments and an appropriate breakup fee.

MNG accused Gannett of stonewalling on deal discussions by refusing to extend a Thursday deadline for board nominations that has been in place for nearly a year. I’m sorry, but if that tactic didn’t work for Bill Ackman at Automatic Data Processing Inc., it’s not going to work here. The deadline is what it is, and if MNG wanted more time to negotiate, it shouldn’t have made its first public bid only about a month beforehand. Of course, if it had bid earlier, it wouldn’t have been able to take advantage of Gannett’s slumping share price in December. MNG attempted to reserve the right to submit placeholder names for its nominees to give it more time to develop a slate, according to the Wall Street Journal. Gannett’s bylaws don’t allow this, but even if they did, it’s a sloppy way to go about a proxy fight.

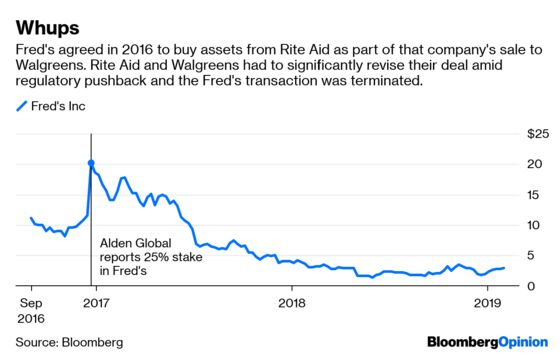

A look at the slate MNG did put forward shows why it wanted more time; the candidates are a mix of current or former MNG executives, Alden Global employees and directors currently serving on the board of drugstore chain Fred’s Inc. Alden Global is the biggest shareholder of Fred’s and its president is the company’s chairman. Most activist investors worth their salt will at most nominate one or two people from their own firm to proxy-fight slates, and they go to great lengths to emphasize that the other would-be directors are independent. The extent to which people believe these protestations of independence is a different question, but it’s important to at least try to maintain the idea that whatever agenda the hedge fund is pushing is for the greater good of all shareholders and not just for its own benefit.

Perhaps more important is the need to put up a slate that’s seemingly better-equipped to manage the company than the current board. Alden Global has boosted the profit margins of its newspaper holdings to meaningfully higher levels than the rest of the industry, albeit at a significant cost to the quality of the product and journalism jobs, as my Bloomberg Opinion colleague Joe Nocera has documented. That makes it a less ideal partner for Gannett than its erstwhile takeover target Tribune Publishing Co., with which it has reportedly rekindled deal talks. In the absence of a higher bid and more concrete information about MNG’s financing capabilities, it’s fair to take a look at what’s happened to Fred’s stock price since Alden Global built a stake in the company and question the merits of the nominees’ operating chops:

The situation offers an interesting contrast to Broadcom Inc.’s hostile pursuit of Qualcomm Inc. Broadcom initially nominated 11 directors to Qualcomm’s board, all of whom were independent on the face of it; the semiconductor company had financing commitments from Bank of America Corp.’s Merrill Lynch arm, Citigroup Inc., Deutsche Bank AG, JPMorgan Chase & Co., Morgan Stanley and Silver Lake Partners for the $100 billion-plus deal; and eventually, it offered to pay an $8 billion reverse breakup fee if regulators rebuffed the deal. It did all of this before Qualcomm offered to enter into a non-disclosure agreement for bilateral due diligence. Broadcom didn’t win the proxy fight because the U.S. government forced the then-Singapore-based company to withdraw its slate over national security concerns. But Broadcom knew what it was doing. It’s hard to say the same about MNG.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.