FX Markets Lull Draws Traders Into a Bet That Went Awry in 2020

FX Markets Lull Draws Traders Into a Bet That Went Awry in 2020

(Bloomberg) -- Once again, currency traders are starting the year by loading up on bets for lower volatility. But it’s already beginning to look a bit too one-sided to last.

In a repeat of an option-market pattern seen since 2017, investors are showing a clear preference for shorting volatility early in the year. The reasoning appears to be the same now as it was then: central banks are expected to refrain from changing their policy mix and to continue with accommodative biases, helping keep currencies in tight ranges over the medium term.

There’s more than one risk to that outlook. For one, bets for dollar weakness could regain traction. Such a view, which dominated much of 2020 and boosted volatility, is based on U.S. twin deficits and expectations for the Federal Reserve to sustain support for some time to come. With the euro and the yuan gaining popularity among global reserve managers and the slower-than-expected global vaccinations now probably mostly priced in, there’s a case for greenback declines to resume.

A dollar rebound would spark volatility, too. Bearish positioning is already stretched in the greenback, which has lost 13% of its value on a trade-weighted basis since March and could regain some ground if coronavirus vaccinations in America accelerate, or if fresh U.S-China trade tensions emerge. Any move in money markets to front-run the risk of future Fed policy tightening would also support the dollar.

Other risks to the short-volatility trade include the possibility that global central banks start communicating concrete plans to exit ultra-easy policies. That could see currencies react sharply, just as they did when some Fed officials opened a debate over tapering asset purchases. And even without tapering, currencies can attract large inflows from fixed-income markets, where yields have been crushed by ultra-easy monetary policies.

READ MORE: World’s Largest Market Is Luring In Yield-Starved Bond Investors

‘Naked’ Options

For now, currency fluctuations remain locked in a narrowing trend. The J.P. Morgan Global FX Volatility Index touched a six-month low last week. Leveraged investors have been selling volatility almost since the year started, according to traders and brokers in Europe. A similar trend was seen at the start of 2020, before the coronavirus crisis spurred a blowout in foreign-exchange fluctuations.

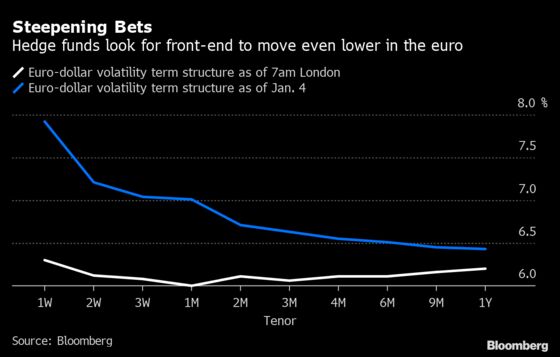

In fact, some hedge funds have been selling so-called naked options in the euro. That would allow them to earn a premium on such sales, but also expose them to theoretically unlimited losses, according to traders familiar with the transactions who asked not to be identified because they aren’t authorized to speak publicly.

Bets against volatility also about in sterling. So-called vega selling interest is picking up in pace, while low-delta options in the yen are facing selling pressure.

According to a Europe-based broker, part of the interest in selling volatility comes from interbank desks that look to avoid so-called theta decay -- in other words, the cost of holding an option for long. Traders at investment banks have been looking to fade the current dip in hedging costs, but are waiting for a better entry point, according to the broker.

- NOTE: Vassilis Karamanis is an FX and rates strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2021 Bloomberg L.P.