PGIM's Tipp Says Future of 10-Year Treasury Yields Is Below 3%

Future of 10-Year Treasury Yields Is Below 3%, PGIM's Tipp Says

(Bloomberg) -- Bond market bull Robert Tipp is quick to admit that the facts have changed, with the strength of U.S. economic growth hitting Treasuries harder than he expected. But they haven’t changed his mind on the downward path for U.S. yields.

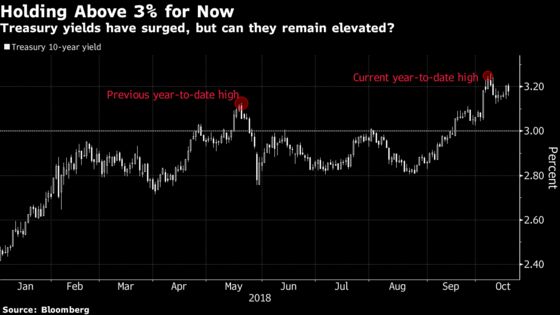

The 10-year Treasury rate, currently around 3.19 percent and close to the seven-year high it reached earlier this month, will be back below 3 percent in the not-to-distant future, according to the head of global bonds at PGIM Fixed Income, which oversees about $716 billion of assets. Central to Tipp’s stance is the sheer weight of global savings set to pressure yields lower, rather than any particularly gloomy outlook for growth. He’s sticking to his view that yields on longer-dated U.S. debt can’t rise much further from here, although he’s wary of calling a peak for this year just yet.

“Looking out a couple of years, I think the 10-year will probably be down around 2.5 percent,” said Tipp, who is based in Newark, New Jersey. Tipp also said he sees potential for the U.S. yield curve to invert by the second half of next year, although he’s not predicting a recession.

Tipp’s stance on Treasury rates moving lower is in contrast to many market observers, who see 10-year yields holding firmly above 3 percent as the Federal Reserve hikes its benchmark and the U.S. government’s ever-growing debt pile adds to supply pressures. The 10-year yield this month climbed as high as 3.26 percent and hasn’t been below 3 percent since its surge higher on Sept. 18.

“The wave of rising debt levels crested and we’re in an environment of an aging demographic and the savings are really spilling over,” Tipp said.

The impact is not limited to the U.S. market, he said. Inexorable demand for longer-maturity bonds means pension funds, financial institutions and sovereign wealth funds are “coming into the euro area and scooping up product,” he said. Meanwhile in Asia, “everything that is attractive or creditworthy to buy has been taken to high levels.”

In Tipp’s view, these kinds of buyers can offset the pullback in demand from the developed world’s largest central banks as they unwind their quantitative easing programs. He’s also not convinced by the argument that the increase in Treasury supply will lead to higher yields, noting that fiscal policy in other places is being tightened even as the approach in the U.S. has loosened.

“The fact of the matter is, outside of the U.S. everyone else is cutting issuance,” he said, pointing to tax increases in Japan and Europe’s campaign to curb spending. So the U.S. Treasury’s increased borrowing is “blending into the woodwork.”

On U.S. growth, Tipp said it’s not surprising that the headwinds of the 2008 crisis should have taken a decade to lift, and that the underlying potential of the American economy may have been underestimated as a result. But the best may already be past.

“It’s a working assumption that the rest of the world has peaked in terms of growth and that the U.S. isn’t going to spin off into a different orbit all on its own, that we’re probably at some kind of a peak of U.S. optimism,” he said. “The market is trying to be measured and not run away with the unabated high rate of growth thesis.”

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Greg Chang

©2018 Bloomberg L.P.