Funds With $2 Trillion Train Their Sights on Europe's Bond Fringe

Funds With $2 Trillion Train Their Sights on Europe's Bond Fringe

(Bloomberg) -- Bond behemoths that manage a combined $2.3 trillion are betting the euro-convergence trade is back.

From Spain to Slovenia, yields on the riskier fringes of Europe’s debt market have narrowed the gap to those of benchmark German bunds from this year’s peak. PGIM Fixed Income and Amundi are betting economic momentum and ECB support will take them even closer.

Investors eager to deploy cash in a risk rally are finding all the encouragement they need in a nascent recovery in China, an extended pause on Fed rate rises and about $10 trillion of bonds globally with yields below zero. Throw in the European Central Bank’s commitment to backstops, and government bonds from Italy, Spain, Portugal and even Greece can start to feel risk-free.

“We’re active in all of the names looking for relative value opportunities,” Robert Tipp, chief investment strategist at PGIM Fixed Income, which oversees about $716 billion, said by phone. “People are put off by the headlines, and as a result have blown past the opportunities there.”

Tipp especially likes bonds from Spain, Italy, and Greece, all of which have outperformed German and French peers in April. Meanwhile the yields on Slovenian bonds have narrowed the gap to those of bunds by 30 basis points since Feb. 8.

Even as yields have been rising across Europe in the past week, for peripheral bonds it’s been at a slower rate than for core debt. And there’s scope for the riskier bonds to get even closer to the benchmark, according to Amundi, which runs $1.6 trillion as Europe’s largest asset manager.

“The ECB’s accommodative stance may favor peripheral bonds and financial credits,” said Eric Brard, head of fixed income at Amundi. “We have allocation in Italy, Spain, and Portugal. We are underweight negative-yielding parts of the European bond market.”

Draghi Deliverance

Peripheral bonds got their latest leg up on April 10, when Mario Draghi said the ECB is ready to “adjust all of its instruments” as appropriate to ensure that inflation continues to move toward its target.

That may not have been as momentous as the “Whatever It Takes” speech Draghi delivered back in 2012 which drove Italian bonds to a whopping 21 percent gain that year. But with Italy mired in recession and Germany’s economy stagnating, it still offered investors plenty of reassurance.

Policy makers have also discussed measures to reduce the effect of negative interest rates on banks such as tiering and new long-term loans. Whether or not they materialize, the ECB has already changed its guidance and now sees rates on hold at least through 2019.

“The idea that the ECB is going to get rates above zero has dropped away, leaving the peripheral curves looking conspicuously high and steep relative to the core markets,” said PGIM’s Tipp.

Pimco Unimpressed

Not everyone is enticed. Pimco, for one, is concerned about the sustainability of Italy’s debt and the illiquidity of Greece’s.

“We remain quite cautious,” said Nicola Mai, a fund manager and sovereign credit analyst at Pimco. “You don’t want to be excessively underweight because the negative carry is significant, but on balance we trade it on the underweight side.”

A combination of national debt at 132 percent of GDP and a recession certainly don’t make Italian bonds sound like a screaming buy. Adding to this is a risk of renewed tensions with the European Commission given the country’s deepening fiscal woes.

Italy also faces risk of a downgrade from S&P Global Ratings, which is due to complete a review Friday. While the nation’s growth and budget outlook have deteriorated, some analysts still expect the ratings to remain unchanged as its debt financing costs fall. Italy’s 10-year yield, above 3 percent during the last review in October, has dropped to 2.69 percent.

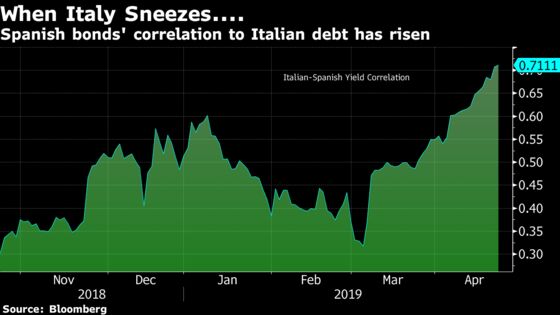

While Pimco judges that Spain’s economic outlook has improved, the asset manager sees contagion from Italy as a risk. The 30-day correlation between Italian 10-year bonds and Spanish debt of the same maturity is holding near an eight-month high, according to data compiled by Bloomberg.

“The Spanish fundamentals are quite a bit better and there could be convergence to core or semi-core over time,” said Mai. “If it weren’t for the sensitivity to Italian markets, Spain would have the potential to compress.”

Spain faces homegrown threats too: A snap election this Sunday could upstage the longest rally in its bonds in four years. It’s even been singled out by former Trump adviser Steve Bannon as the next domino to fall as populism spreads in Europe, though Prime Minister Pedro Sanchez is favored to win.

For many investors, those shortcomings are worth overlooking in exchange for higher returns. Hunkering in German and Swiss securities means accepting negative yields -- and losses if held to maturity. Yields on 10-year bunds fell back below zero on Wednesday and reprised their lowest level in two weeks.

Political uncertainty could rattle Spanish bonds in the near term, according to Paul Brain, head of fixed income at Newton Investment Management, but it won’t change the bigger picture of convergence backed by fundamentals and the hunt for returns.

Since the Fed’s dovish pivot, the push to risk has overtaken the pull to safety across markets. The S&P 500 hit a new record this week, while global high-yield bonds have handed investors 7.3 percent in 2019. Signs that China will avoid a hard landing and optimism about a detente in trade tensions with the U.S. are helping fan the flames.

Even Cyprus, forced to seek an international bailout just six years ago, found investors clamoring to participate in a sale of bonds this week. The Mediterranean island nation drew an order book of more than 6.3 billion euros ($7 billion) for 750 million euros of 30-year notes and pared back initial yield indications by quarter of a percentage point, according to managers of the sale.

The risk rally “doesn’t feel like something you want to fight right here,” Bob Michele, chief investment officer at JPMorgan Asset Management, said in an interview with Bloomberg TV Tuesday. “While it’s tempting to take profits and wait for some pullback to get back in, it means you have to get two things right. Why go through all of this? Just enjoy the ride.”

To contact the reporters on this story: Anchalee Worrachate in London at aworrachate@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Cecile Gutscher

©2019 Bloomberg L.P.