Fed Carries Funding Markets Over Quarter With Rocky Path Ahead

Funding Markets Becalmed by Fed Turn to a Murky Third Quarter

(Bloomberg) -- U.S. funding markets are approaching quarter-end on a remarkably sure footing, given the Treasury is still borrowing in near-record amounts, its cash pile has barely ever been larger, and the pandemic appears to be seeing a resurgence.

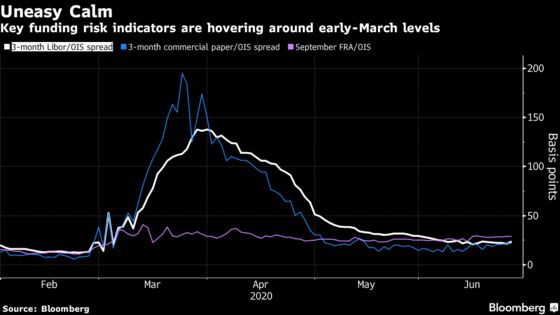

Even as Libor jumped the most in three months Thursday, indicators of stress in this crucial corner of financial markets -- such as the spread between three-month Libor and the risk-free rate -- are hovering where they were before the March upheaval. In secured funding markets, the benchmark repurchase rate remains in check, and the Federal Reserve’s overnight liquidity facilities have hardly been touched this week.

That all adds up to a big win for the Fed, though maybe not exactly mission accomplished. It’s a testament to officials’ swift and aggressive actions over the past three months that this key market is calm at what would typically be a volatile time, with banks wrapping up their books at mid-year.

The threat of a relapse heading into the second half of 2020 is reduced with ample cash in the system. The biggest risk to this hard-won equilibrium is if demand is unable to keep up with the Treasury’s borrowing needs, with more government stimulus potentially on the way.

“The really big unknown right now is that we’re at this fork in the road as far as stimulus goes,” said Blake Gwinn, a rates strategist at NatWest. “That will have a massive impact on bill supply and funding needs.”

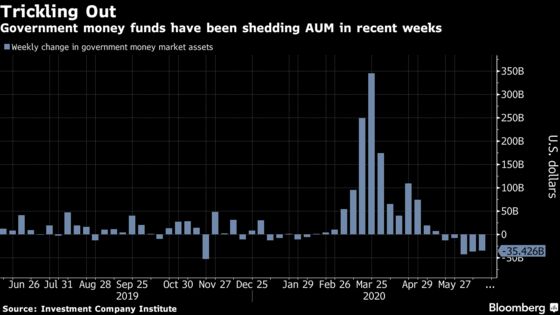

There are signs that buyers might be starting to drift out of the safety of bills, even as supply may need to ramp up again. In particular, strategists have been eyeing outflows from government money-market funds.

While the Treasury’s cash hoard, at a near-record $1.61 trillion, has allowed it to trim bill supply, Gwinn doesn’t see major cuts on the way. Spending needs may surge again soon enough, as the administration is reportedly considering a $1 trillion infrastructure package.

There were concerns in recent weeks that the Treasury’s cash stockpile could complicate matters for the Fed at quarter-end, because of the potential for increased volatility in reserves at a time when short-term funding needs are typically more acute.

That hasn’t turned out to be the case. For one thing, the Treasury’s cash pile has dropped from last week’s historic level. Also, unlike September, when large flows tied to corporate tax payments and Treasury auction settlements crashed a system that was running close to scarcity, reserves are now abundant. That’s thanks to asset purchases and a plethora of liquidity facilities that have expanded the Fed’s balance sheet beyond $7 trillion.

“When the Fed started blowing out its balance sheet, reserves really ceased to matter,” Gwinn said. “We’re so far past that, we’re so far into reserve abundance.”

Stress indicators in the U.S. are muted so far. Three-month Libor did fix higher Thursday, in the biggest increase since March, but it’s coming off a five-year low and returning to last week’s level. The spread to overnight index swaps, the risk-free rate, rose only a fraction.

To Jon Hill, U.S. rates strategist at BMO Capital Markets, that suggests upward pressure on the benchmark “will not be durable absent a sharp correction in risk assets.”

As for secured funding markets, “heading into quarter-end, additional repo pressure could mount, but their spillover into other areas of funding markets is unlikely,” according to a report from Steven Zeng and Craig Nicol, strategists at Deutsche Bank AG.

The markets are “functioning well without any major dislocations” in Treasury, mortgage-backed and municipal bond markets, they said in a report dated June 18. Treasuries are maintaining a stable spread to swaps across different maturities, “suggesting stable investor demand despite increased issuance.”

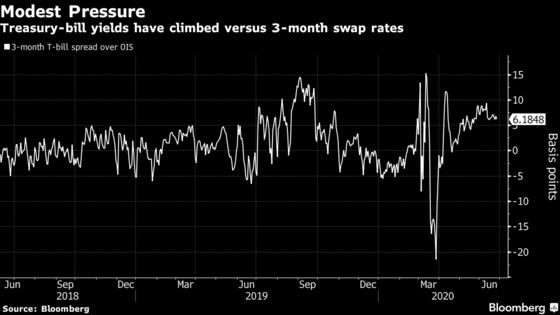

Though that spread measure has jumped around somewhat in the past week, the gap between three-month T-bills and the overnight index swaps rate is still below its peak this month, and well short of the stresses seen in March and April.

Overseas, some stresses remain. The European Central Bank announced plans for a precautionary facility to provide euros to central banks outside the currency area to help ease any liquidity crunches that remain in the wake of the pandemic. And liquidity in foreign-exchange markets is still below norms, according to Guy Debelle, deputy governor of the Reserve Bank of Australia and head of the Global Foreign Exchange Committee.

NatWest’s Gwinn says that even if the course of the pandemic takes a more critical turn, exerting renewed pressure on the economy, the financial system is far better placed now to handle the risks.

“There’s a fuller understanding now of the Fed’s tolerance for funding rates to widen out,” he said. “When we went into this in March nobody had any clue that the Fed would act as quickly and as strongly as they did -- now we know what their playbook is.”

©2020 Bloomberg L.P.