From NYC to San Francisco, Idled America Brings Fiscal Hit

From NYC to San Francisco, America’s Shutdown Brings Fiscal Hit

(Bloomberg) -- In New York City, the virtual shutdown from the coronavirus pandemic is threatening to create massive holes in the budget as billions of dollars in tax revenue disappears. On the other side of the country, the stock market crash may imperil much of the savings California socked away during the economic expansion that now seems poised to end.

Public transportation systems from New Jersey to San Francisco are swiftly losing riders -- and their fare dollars. Airports are seeing fee revenue tumble, as are museums and darkened stadiums. Major financial hits are also being dealt to agencies like Chicago’s Metropolitan Pier and Exposition Authority, which runs the nation’s biggest center for conventions -- another business that has disappeared virtually overnight.

No one has a handle on how vast the toll will be on the nation’s local governments as much of the U.S. economy grinds to a halt, leaving it a near certainty that the nation is heading into the first recession in over a decade.

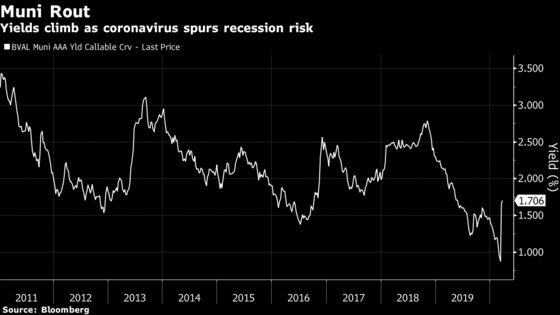

But the unprecedented uncertainty of how long and severe it will be is wreaking havoc in the $3.9 trillion municipal-bond market, which is usually a haven from financial market turmoil. Investors are pulling out their cash, bond prices are sliding, and even the potential for states and cities to raise funds is temporarily drying up as Wall Street banks put new debt deals on hold.

“It’s been a crazy two weeks,” said Debra Crovicz, a managing director at Chilton Investment Co. “People are trying to stay ahead of perceived risk right now. This is going to be a ripple effect through the entire economy.”

By some measures, states are well prepared to weather a brief recession, since many have been building up their reserves during the last several years. By last spring, they had nearly $70 billion in so-called rainy-day funds, according to the National Association of State Budget Officers. Still such savings can run out fast: During the last recession, states’ general-fund revenue tumbled from $680 billion in 2008 to about $610 billion two years later. The tax collections didn’t fully recover for years.

The nationwide shutdown has gathered speed so rapidly over the past week that Wall Street has struggled to get a handle on it. On Monday, the six counties of the San Francisco Bay Area ordered residents to stay home, bringing the nation’s tech center to a standstill. New York Mayor Bill de Blasio floated the idea for the most-populous U.S. city, even if it was dismissed Tuesday by the governor.

New York City comptroller Scott Stringer said Monday the city could “conservatively” lose $3.2 billion over the next six months and most agencies should brace for cuts. His counterpart in Albany, Thomas DiNapoli, said the state’s loss could be as much as $7 billion.

Most officials have yet to put numbers on the impact. Many, including those from California, say they will revise budget forecasts next month. The most populous state has about $21 billion in various reserve funds, a substantial buffer, but that still falls short of the amount needed to minimize cuts in a moderate recession, according to the nonpartisan Legislative Analyst’s Office. On Monday, California lawmakers approved an emergency $500 million spending package to help combat the pandemic, and an additional $100 million for schools.

Local governments will also see sales-tax collections dry up from the closure of restaurants and other businesses. While outright defaults remained rare even during the last recession, investors have been pulling out their money, driving the municipal market into its worst rout since 1987.

The fallout won’t be felt equally. Wells Fargo Securities economists said in a note to clients that Orlando, Las Vegas and Hawaii are among “those likely to be disproportionately impacted.”

“With closings and cancellations now spreading across the nation, the impact may fall heaviest on areas most dependent upon travel and leisure, where lost business is difficult to recoup,” they wrote.

At least 20 events have been canceled at Chicago’s McCormick Place campus and more are expected after Governor J.B. Pritzker banned gatherings of 50 or more people on Monday, said Cynthia McCafferty, a spokeswoman for the Met Pier authority that owns the convention center. Met Pier bonds maturing in 2050 traded for an average of 95 cents on the dollar Tuesday, down from 112 cents on Feb. 24, according to data compiled by Bloomberg.

Travel Blow

Among the bonds that have dropped the most are those backed by airports and airlines’ terminal payments as major carriers deeply cut back the number of international flights. A 5% bond backed by American Airlines due in 2031 related to the construction of its terminal at New York’s John F. Kennedy International Airport traded at a yield of 5.1% Tuesday, compared with 2% in January, according to data compiled by Bloomberg.

The loss of passengers is hitting transit systems hard as more businesses encourage or require employees to work from home and schools shutter. Governors of New Jersey, New York and Connecticut on Monday announced mandatory closings of non-essential businesses, limited restaurants to take-out service and capped social and recreational gatherings at 50 people.

Even before the stepped-up directives to reduce crowds to curb the spread of the virus, ridership was down nearly 19% on New York City subways on March 11 compared with a year earlier, while morning commuters on the Metro-North Railroad fell 48% on March 12, according to the Metropolitan Transportation Authority.

The drop off has already started to negatively affect the MTA’s finances, and there will be “material adverse impacts on the revenues and overall financial condition of the MTA” if the situation deteriorates further, according to a filing to bondholders last week.

“Historical U.S. municipal credit trends are reassuring,” Matt Fabian, partner at Municipal Market Analytics, wrote in a note Tuesday, “but the size and speed of the coronavirus’ economic effects -- led by projections of tens of thousands of American deaths (and some scenarios are much worse than that) -- could effect permanent shifts in domestic and global behavior, making things less predictable in the long term.”

©2020 Bloomberg L.P.